Hey, it’s Marc

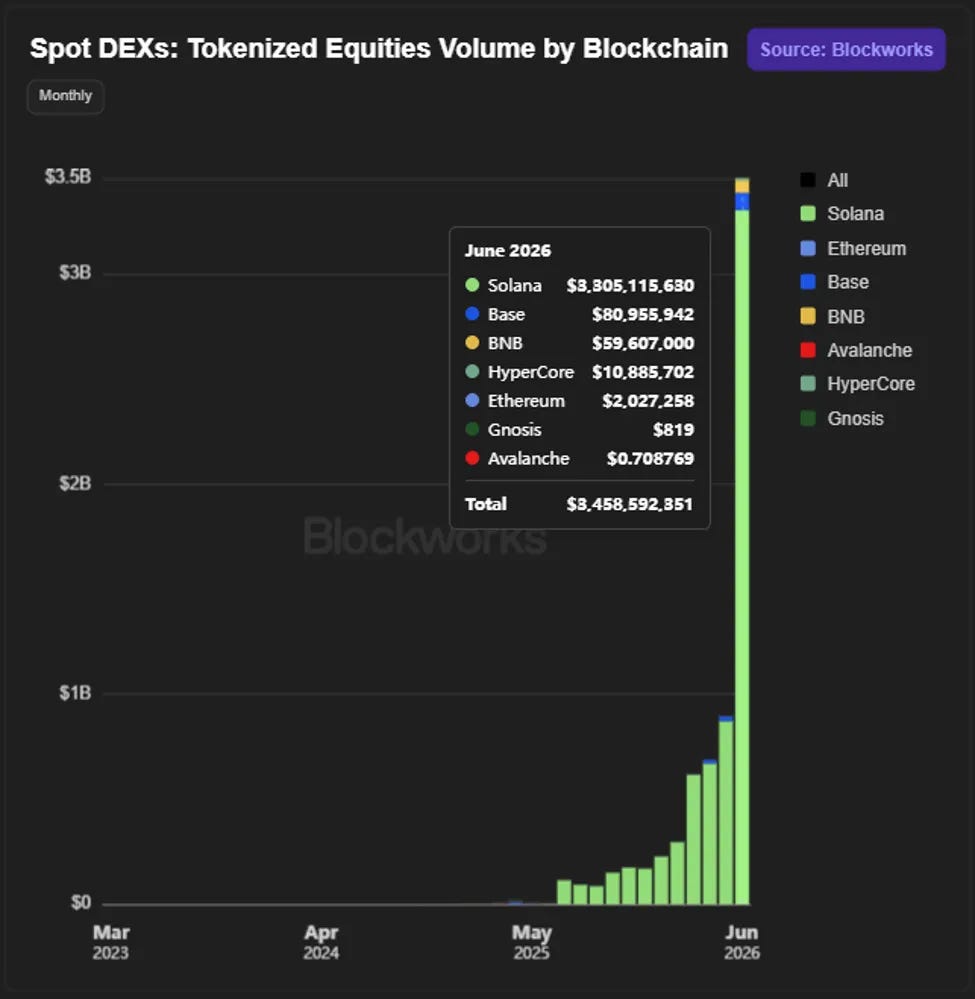

One number stopped me this week: tokenized equities just hit an all-time high of $3.86B in monthly volume, up 145% in a month, while SOL, the chain settling 95% of it, trades at December 2023 prices.

What strikes me most:

Usage is exploding, and the value is flowing to the plumbing rather than the tokens.

For ten years this industry priced tokens as the prize and licenses as overhead.

This week showed that the tides are turning:

Kraken paid $600 million largely for licenses to assemble a bank

Sony committed $40 million for a US bank charter.

SWIFT’s shared blockchain ledger ready with 17 global banks piloting 24/7 settlement

And the quiet confirmation sits in a Broadridge release almost nobody read: its distributed ledger repo platform processed $7.5 trillion in June, arguably the largest production blockchain application in finance. It has no token at all.

And more signals:

And 8+ more signals below.

the poll from last week: most of 51 readers think that OpenUSD will win the stablecoin war.

51 Signal: Tokenized equities hit $3.86B in monthly volume

Top Boardroom Reads & Data

Tokenization Can Change the World’s Financial Architecture (IMF, Tobias Adrian, July 2026). The IMF’s most senior markets official argues tokenization shifts risk from bank balance sheets to the infrastructure operators running the ledgers, which is exactly where regulation isn’t looking yet.

Statement on the 2026 Regulatory Agenda (SEC Chair Paul Atkins, July 2026). The SEC put three crypto rules on its 2026 agenda, covering crypto capital raising, custody and tokenized-securities trading, all targeting proposed rulemakings as early as this month.

The Great Wealth Transfer Is Already Reshaping How Americans Spend (Visa Business and Economic Insights, July 2026). Visa sizes the boomer-to-millennial wealth transfer at $36T over 20 years but finds only ~$8T becomes consumer spending; the rest lands in assets, the pool tokenized products are chasing.

Announcing Our Fourth Fund (Paradigm, July 2026). The largest crypto VC raised $1.2B and explicitly widened its mandate to AI and robotics, the clearest data point yet that crypto-native capital sees its next returns beyond crypto.

Distributed Ledger Repo Processes $7.5 Trillion in June (Broadridge, July 2026). Tokenized repo did $357B a day in June, up 68% year over year, making DLR arguably the largest production blockchain application in finance and nobody talks about it.

🚨Save your spot for our next webinar, space is limited.

I’m sitting down with the people dvising the banks and building the stablecoin rails those banks will plug into.

For CEOs, board members, and heads of strategy at banks, FMIs, asset managers, and custodians.

📅 23 July, 11am EST

🚨 Space is limited. RSVP to secure your spot.

SWIFT just built the banks’ blockchain

What happened: SWIFT announced its shared blockchain ledger is ready for use, built in nine months, with 17 banks across six continents set to pilot tokenized cross-border payments: ANZ, BNP Paribas, BNY, Citi, DBS, HSBC, MUFG, Standard Chartered, UBS and Wells Fargo among them. The goal is 24/7 settlement on trusted shared infrastructure. The same week, UBS completed its first live cross-border stablecoin B2B payments with partner Merge, settling from Switzerland in under two minutes.

51 View: For a decade the question was whether banks would come to public chains or build their own. SWIFT just answered it: they’ll do both, but the coordination layer will be theirs. This is the empire striking back. Stablecoins proved the demand for 24/7 dollar settlement, trillions of dollars of it a month, and SWIFT is now repackaging that exact product inside the correspondent banking trust model. We think the pilot-to-production gap is the whole game. SWIFT ships slowly and governance-first, while Kraken, Circle and the stablecoin rails ship weekly. If the 17 banks are settling real client volume by mid-2027, banks keep cross-border money. If not, this becomes the ledger equivalent of their 2017 DLT pilots.

Be Smart: When someone says “SWIFT is doing blockchain now,” the sharp question is: settlement in what asset? A shared ledger still needs tokenized central bank money or deposits to settle. Whoever supplies that settlement asset, not the messaging layer, captures the economics.

Vanguard blinked

What happened: Vanguard, the $12T asset manager that famously refused to list crypto ETFs, opened a search for its first head of digital assets. The role reportedly covers a multi-year roadmap spanning tokenization, stablecoins and custody. CEO Salim Ramji, who ran iShares at BlackRock when it launched the largest bitcoin ETF, has been in the seat since 2024. To be precise: this is a hiring search, no product has been announced.

51 View: The last major allocator holdout is now recruiting for the thing it swore off, and we think the tell is the job description. It reportedly leads with tokenization and stablecoins, with trading nowhere in sight. Vanguard isn’t warming to bitcoin, it’s conceding that funds themselves are being re-platformed, and a $12T manager cannot sit out the format change even if it sits out the asset class. Our read: Vanguard’s first shipped product is a tokenized money market or index share class, and its crypto ETF stance survives another year as cover while the real migration happens underneath it.

Saylor sold the low

What happened: Strategy sold 3,588 BTC for $216M across the week ending July 5, its largest bitcoin sale ever, in two tranches of 1,363 and 2,225 coins. Proceeds fund the dividends on its five preferred stock series. The company still holds 843,775 BTC plus $2.55B in cash, but this is the second consecutive week of selling and a sharp acceleration.

51 View: Last week’s issue showed the treasury cohort buying the 2026 low. The biggest of them all is doing the opposite, and both can be true because Strategy is no longer really a treasury company. It’s a leveraged fund with fixed obligations: the preferreds pay out whether bitcoin cooperates or not, and with the stock trading near the value of its coins, selling BTC beats issuing equity. We think this is the first structural seller the bitcoin market has ever had at the top of its own cap table. Watch the ratio of coins sold to dividends owed; if it rises while BTC stays flat, the flywheel is running in reverse.

Kraken is assembling a bank piece by piece

What happened: Kraken’s parent Payward closed its $600M acquisition of Reap on July 1, adding global card issuance and stablecoin settlement infrastructure. Six days later, Reuters-reported filings showed Kraken pursuing a full EU banking license through Lithuania. Kraken is already the first digital-asset company on the Fed’s payment rails, live since March.

51 View: Put the pieces in order: Fed payment rails in March, card issuance and settlement in July, an EU bank charter in progress, and a reported IPO ahead. That’s a bank org chart being assembled in public, and I think the sequencing is deliberate: infrastructure first, charter second, listing last, so the prospectus reads “regulated global bank with an exchange attached” rather than “crypto exchange seeking respectability.” The margin logic is simple: Exchange fees compress every year, while deposits, cards and settlement float don’t. We expect at least one more top-five exchange to file for a banking charter within twelve months, and the interesting question is whether regulators price that approval like a fintech or like a bank.

News Flashes

(deduplicated — nothing here is a Signal above)

Infrastructure and Markets

Brazil’s B3 introduced options on bitcoin, ether and solana futures, extending Latin America’s most complete regulated crypto derivatives suite.

Gemini launched commission-free US stock trading, its next step from crypto exchange to broker-dealer super app.

Regulation and Policy

Sony Bank won conditional OCC approval for Connectia Trust, a US stablecoin trust bank with $40M capital targeting a 2027 launch under the GENIUS Act.

Coinbase secured UK authorization to offer equities and derivatives alongside crypto, its biggest UK expansion since entering the market.

Banking and Payments

PayPal’s PYUSD went native on Polygon via Paxos, joining a network settling $2.5B in stablecoin volume daily.

Hyundai Card completed its first live stablecoin remittance between Hyundai Motor’s US and Mexico units using USDT on Avalanche, cutting a 3-4 hour transfer to seven minutes.

Funds, Deals and Others

Gauntlet raised a $125M Series C from sole investor SBI Holdings to expand institutional DeFi risk management into yen and peso stablecoins.

Tether invested $20M in Brazil’s Mercado Bitcoin, a 4.5M-user platform with more than 10 financial licenses across Brazil and Europe.

The Machine Layer

Paradigm raised a $1.2B fourth fund expanding beyond crypto into AI and robotics, backing Zipline, True Anomaly and Nous Research alongside Hyperliquid and Tempo.

Meta is preparing to sell excess GPU capacity as a cloud provider, monetizing part of its $125B+ 2026 capex the way Amazon once monetized spare servers.

Anthropic’s reported ~$47B revenue run-rate has passed OpenAI’s $25-33B, reshuffling the AI leaderboard mid-cycle.

51 View: The one that matters is Anthropic passing OpenAI. A year ago this ranking looked settled. Now the challenger runs at a reported ~$47B annualized against OpenAI’s $25-33B, and the flip happened without OpenAI shipping anything visibly worse. That is the tell: enterprise AI spend moves to whichever model wins the current eval cycle, so leadership rotates with every model generation. We think run-rate has become a lagging indicator at the model layer. The durable assets are contracts and distribution, and that race is still wide open.

Watchlist / On the Calendar

What to prepare for:

July 28-29, FOMC meeting. Markets price 75% hold, 25% hike. A hike would be the first test of whether the license-swap builders keep shipping into genuinely tightening money.

This month, SEC crypto rule proposals. All three agenda items (offerings, custody, market structure) target notices of proposed rulemaking as early as July.

Mid-July , Q2 earnings. Coinbase and Strategy report; watch whether Strategy discloses more BTC sales and how Coinbase frames its UK equities launch.

Late July, Hyundai Card’s Europe pilot. Round two runs on various local currencies with Visa and Circle participating.

End of July, Bank of Korea government-fund disbursement test. Public spending on tokenized rails, the first sovereign use case at scale.

August 31, Revolut delists USDT for EEA users. Deposits stop July 30; the biggest retail distribution loss yet from Tether’s MiCA refusal.

Mid-2027, SWIFT ledger production volume. The falsifiable test of this week’s headline signal.

One Quick Favor

You asked for more contrarian takes and we leaned in again this week (Saylor as a structural seller, SWIFT as the empire striking back). Tell us where to push next:

51 Intelligence Stack: Related Reading

📊 Issue 185: 140 companies vs. Circle — The treasuries bought the low that Strategy just sold into.

📊 Robinhood just rented a bank — The other side of the license swap: brokers building banking without charters.

📊 Tokenized stocks’ first $3B month — Why Coinbase and Gemini want equities licenses right now.

That’s all for now, folks.

– Marc & Team