Hi, it’s Marc. ✌️

Brent Johnson has spent roughly 25 years in financial markets, and he has one of the cleanest frameworks afor thinking about the dollar. Back in 2018, when the "de-dollarization" narrative was just starting to simmer, he stepped onto the global stage with a theory that sounded almost arrogant at the time. He called it the Dollar Milkshake Theory.

But one phrase that made me more curious was:

“Stablecoins are a stealth weapon of empire. They are quietly re-dollarizing the world from the bottom up. They do something no military base or trade agreement ever could.”

That is a strong phrase, but in this conversation, it was not used for effect. It was used as a description of what is already happening. The logic is straightforward. If people around the world want to hold dollars, but they want them in a form that is faster, cheaper, and easier to move than the legacy banking system allows, stablecoins become the obvious answer. And because dollar stablecoins have to be backed by dollar assets, that creates new demand for U.S. Treasury securities.

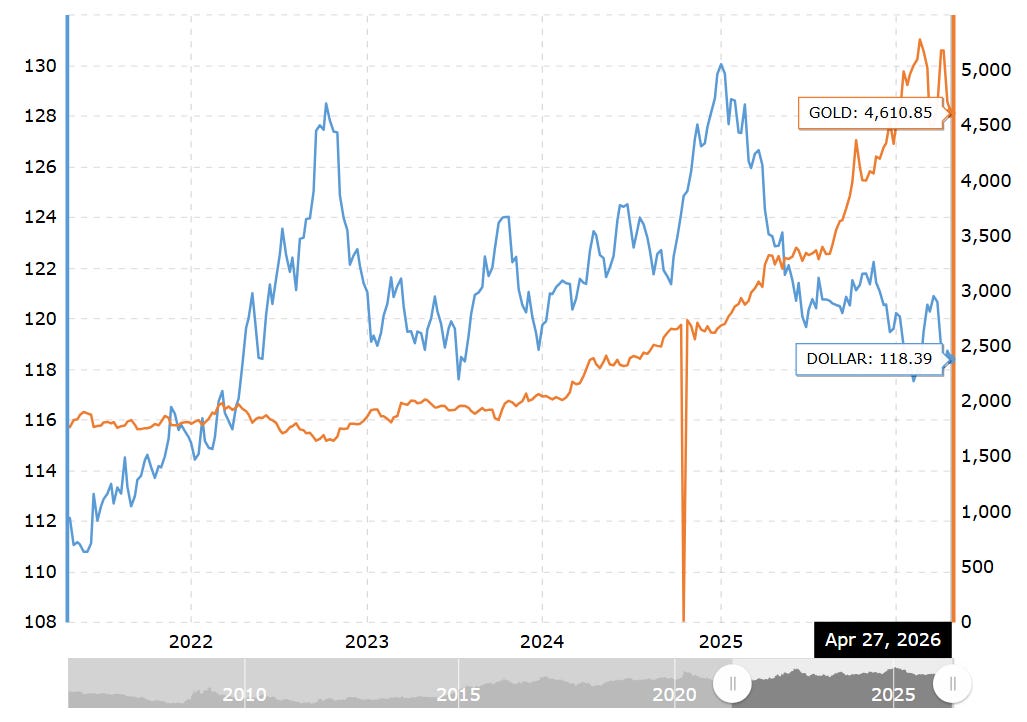

Dollar Milkshake Theory, a framework he first laid out in 2018 that argued, against almost universal consensus at the time, that the U.S. dollar would strengthen precisely as the rest of the world printed more money. It was controversial then. It looks prescient now. The DXY is hovering around 99.66 even as gold has already crossed $5,000, which is, strangely, exactly what Brent said would happen.

So I sat down with him to ask the next question. Now that the milkshake thesis has largely played out, what is the new chapter? And where do stablecoins, tariffs, a $39 trillion national debt, and a potential sovereign crisis all fit together?

His answer was one of the most coherent explanations I have heard of, where the dollar actually goes from here, and why the U.S. government’s decision to let private companies issue dollar-backed stablecoins may be the smartest geopolitical move of the decade.

About Brent: Brent Johnson is the founder and CEO of Santiago Capital, a San Francisco-based registered investment advisor founded in 2011. He holds an MBA in International Business from the Thunderbird School of Global Management and began his career as an auditor at Philip Morris before moving through Donaldson, Lufkin & Jenrette in New York City. He has spent roughly 25 years in global macro markets and is the creator of the Dollar Milkshake Theory, first articulated publicly in 2018. Alongside his RIA practice, he runs a standalone institutional research subscription at research.santiagocapital.com. In June 2025, he joined Monetary Metals' advisory board, advising on the distribution of gold-backed fixed-income products, including gold leases and bonds. He hosts a weekly show called Milkshakes, Markets and Madness on YouTube.

🚨We’re opening sponsorships for our next podcast series. Top guests. Serious listeners. Claim your spot →

🎧 Jump to the best parts

02:37 Understanding the Dollar Milkshake Theory

05:38 The Relationship Between Inflation and Dollar Strength

08:27 The Role of Gold in the Dollar Milkshake Theory

11:00 Stablecoins as a Stealth Weapon of Empire

16:16 The Global Demand for Stablecoins

21:51 Bitcoin’s Role in the Financial Landscape

27:10 Potential Sovereign Debt Crisis

32:29 Looking Ahead: Economic Outlook and Global Events

Important Links

Website: https://santiagocapital.com/about/

LinkedIn: https://www.linkedin.com/in/brent-johnson-40a8461/

YouTube: https://www.youtube.com/channel/UChvlmVy6Q0a9uC1jRFRpp8Q

Watch or listen now:

YouTube • Apple Podcasts

Our biggest takeaways from this conversation:

1. The milkshake was never about the dollar being great, it was about everything else being worse

When Brent first presented the Dollar Milkshake Theory in 2018, most people in macro were calling for dollar decline. The argument against him was simple: the U.S. had too much debt, was printing too much money, and the world was moving toward alternatives. He was not arguing against any of that. He was arguing that none of it mattered if everyone else was in worse shape.

The name itself comes from the film There Will Be Blood, in which an oil executive tells a rival landowner that he does not need to buy the land to get the oil beneath it. He just puts his straw in from his side of the fence.

“The United States has the straw. And when the rest of the world prints money, the United States sucks up all that capital into their own markets.”

That is largely what happened over the following six years. The U.S. attracted more foreign capital than any other country in the world. The Fed raised rates from zero to five percent in under a year, something many observers said was impossible without breaking the economy. It did not break it, at least not in the way people expected. And through all of it, the dollar stayed stronger than almost anyone predicted.

The most common misreading of the theory, Brent says, is that people thought he was predicting dollar strength at the expense of everything else. He was not.

“I never said the dollar was going to go higher and everything else was going to collapse. I said the dollar would go higher, but gold would go higher, that U.S. equities would go higher, that U.S. dollar assets would go higher.”

His original price targets were a DXY of 150 and gold at $5,000. Gold hit $5,000. The dollar never reached 150, it peaked around 114 in 2022 and currently sits near 99.66. By his own accounting, the gold call was a 400% return from where he made it; the dollar call was a 50-60% move. He never claimed the dollar would outperform gold. Most of his critics did not notice that distinction.

The deeper point is the difference between relative strength and absolute purchasing power. The dollar can be losing value against real goods while simultaneously rising against every other currency. Both things are true at once.

“You can have a rising dollar on a relative basis, but still have it lose purchasing power versus real things. And this is something that people need to understand, when I talk about a strong dollar, I don’t mean your purchasing power. What I mean is versus foreign currencies.”

This matters enormously if you live outside the United States. When the dollar strengthens, every country that has to import goods or services dollar-denominated debt feels the squeeze, often violently. The U.S. middle class might feel richer on paper, while people in Turkey, Argentina, or Nigeria find that their savings have quietly been cut in half.

Related podcast and reads:

How the U.S. Weaponized the Dollar (And Stablecoins), with Eddie Fishman, New York Times Bestseller

2. Gold ultimately wins, but you still need dollars to operate right now

Brent is not against gold. He thinks gold is the ultimate beneficiary of the global monetary system’s dysfunction.

“The dollar doesn’t ultimately win. Gold ultimately wins. So for anybody who needs to hear me say that again, gold is the ultimate winner of the milkshake. But in the short term, you still need dollars to operate on the global stage.”

The proof of this showed up in real time during the recent escalation in the Middle East. As the Strait of Hormuz disruptions sent oil prices sharply higher, gold and silver pulled back. So did Bitcoin. The reason was: countries that needed to buy now-expensive energy had to sell whatever they held to get dollars first. The mechanism was visible, live, in the market.

“Those who needed to transact on the global stage had to sell their gold to get dollars to buy the oil that was now priced 50% higher than it was a month ago. And I think that’s a demonstration that to operate on the global stage, you still need dollars.”

Gold going to $10,000 is still possible in Brent’s view. But a voluntary return to the gold standard is not. Governments will not willingly put financial handcuffs on themselves, because a gold standard limits how much they can spend, and politicians do not win elections by saying no.

“If governments did go back to a gold standard, they would have to massively devalue their currencies against gold when they did it. A lot of people would lose all of their savings. And once they had that constraint, their gold holdings would put a restriction on how much money they could spend. But politicians get elected by saying yes.”

If a gold standard ever comes back, Brent believes it will be forced on governments from the outside, not chosen. A reset after a crisis, not a planned reform.

Related podcast and reads: