MoonPay, Iron, and the Stablecoin Endgame

In February 2025 Stripe acquired Bridge for $1.1B. A few months later, in March 2025, MoonPay acquired Iron, a German stablecoin infrastructure company, for a reported $100M+.

Stablecoins are having their moment. And this time, it’s not hype.

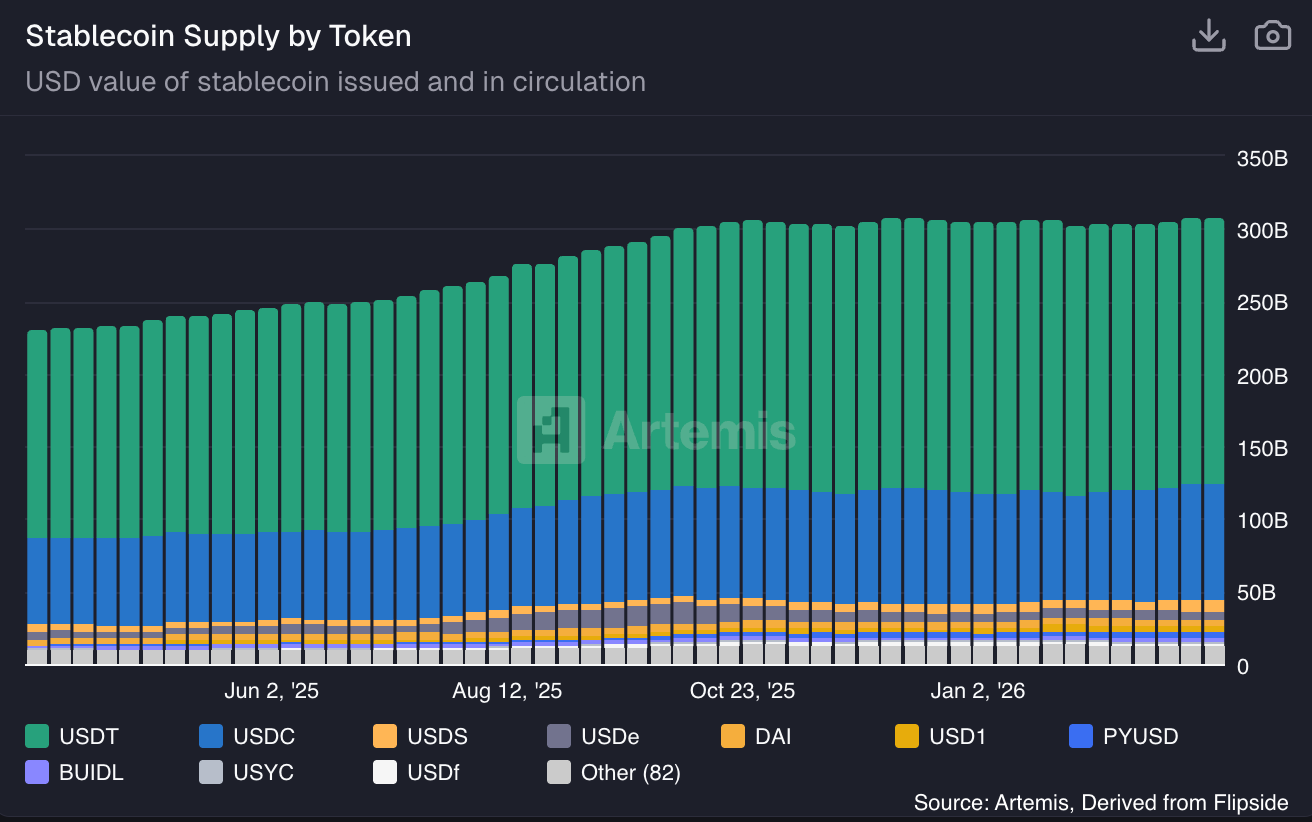

Supply exceeds $310 billion. Monthly volumes run into the trillions. What began as a crypto workaround now looks more like financial plumbing.

In February 2025 Stripe acquired Bridge for $1.1B. A few months later, in March 2025, MoonPay acquired Iron, a German stablecoin infrastructure company, for a reported $100M+.

It was MoonPay’s second acquisition in just 60 days, following its $175M purchase of Helio, Solana’s top payments processor, now known as MoonPay Commerce.

The shift in focus was clear. This was not about trading apps. It was about rails.

“This is our Braintree moment,” said MoonPay CEO Ivan Soto-Wright, referencing PayPal’s game-changing leap into payment infrastructure.

The comparison was deliberate. PayPal’s acquisition in 2013 moved it up the stack. Stablecoins are entering a similar phase. The contest is no longer about who owns the wallet. It is about who owns the wiring.

The floodgates opened in July when President Trump signed the GENIUS Act into law, creating the first federal framework for dollar-pegged stablecoins. Within days, Bank of America’s CEO confirmed the bank is exploring stablecoin issuance. JPMorgan launched JPMD on Coinbase’s Base blockchain. Deutsche Bank, Citi, Wells Fargo, Amazon, and Walmart are all reportedly making moves. Stablecoin market cap surged past $300B.

Translation: The financial stack is being rebuilt. Quietly. Globally. With stablecoins.

And with the GENIUS Act passed and MiCA living in Europe, the window for building defensible positions is shrinking fast.

The prize? Cross-border B2B payments represent trillions in annual volume, where PSPs and Fortune 500 treasuries are finally realizing that wire transfers taking days and costing 3-5% aren’t competitive when stablecoins can settle in seconds for sub-1%.

Today, we break down why this matters, why stablecoin infrastructure is where the real value will accrue, and why the next 24 months will separate the winners from everyone else.

P.S. We spoke directly with Iron’s co-founder and CEO, Max von Wallenberg, in a recent interview to inform this piece. His perspective and quotes are included throughout.

Why Now: The Stablecoin Moment

After a decade in crypto, we’ve watched countless promises of “mainstream adoption” come and go. And this is the first time we can say, with conviction, it’s different. 2025 was the year stablecoins crossed the chasm from experimental technology to core financial infrastructure, with 2026 confirming their place as the internet’s default settlement layer for global payments.

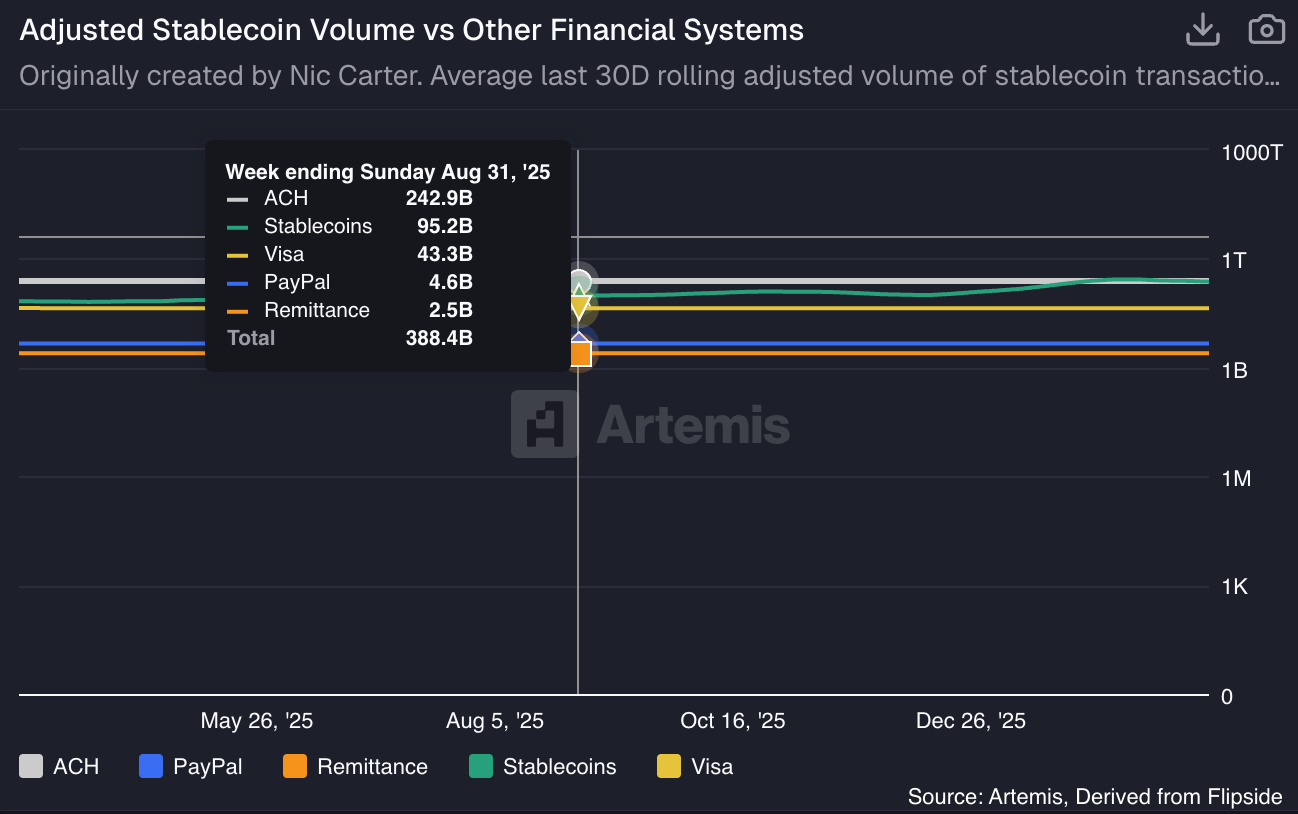

As of February 2026, over $310 billion in stablecoins circulate globally, facilitating more than $10.3 trillion in monthly volume (Jan 2026). But the number that matters most? Since Q1 2025, stablecoins ($140.5B adjusted volume) have been processing more volume than Visa ($43.3B). Stablecoins moved $46T in the past year, up 106% and are projected to dwarf that number.

This is a paradigm shift driven by three converging forces: regulatory clarity, enterprise adoption, and infrastructure maturity.

The Regulatory Catalyst

In July 2025, President Trump signed the GENIUS Act into law, creating the first federal framework for dollar-pegged stablecoins. Treasury Secretary Scott Bessent was explicit about the strategic intent: “We are going to keep the U.S. the dominant reserve currency in the world, and we will use stablecoins to do that.”

Later in the year, the SEC provided equally important clarity: digital dollars used for payments, fully backed 1:1 by real assets, are not securities. This removed significant regulatory uncertainty and signaled openness toward widespread institutional adoption.

Europe implemented MiCA. The Netherlands became an early focal point for licensing under the new regime. Hong Kong launched its stablecoin framework. The direction was consistent, stablecoins would be regulated as financial infrastructure.

The Enterprise Wake-Up Call

Something shifted in early 2025. Within the span of months, billion-dollar acquisitions, major IPOs, and product launches from the world’s largest banks and payment processors signaled that stablecoins had crossed from crypto-native experimentation into mainstream financial infrastructure.

As Jess Houlgrave, CEO of Reown, put it in our recent report: “We’re watching a shift happen in real time. Stablecoins aren’t fringe anymore, they’re quickly becoming the default way users expect to transact on-chain and soon millions of non-crypto native users will be using stablecoins under the hood of applications without even knowing it.”

Max von Wallenberg, co-founder and CEO of Iron, describes it as a the “PSP stamp of approval” effect: once the first major payment processors placed billion-dollar bets on stablecoins, the rest of the industry couldn’t afford to wait.

And the pace has been remarkable. The timeline from Money Movement 2.0 tells the story:

February 2025: Stripe acquired Bridge

March 2025: MoonPay acquired Iron

May 2025: JPMorgan, Bank of America, Citigroup, and Wells Fargo explored a joint stablecoin

June 2025: Circle completed its landmark IPO; Shopify integrated native USDC payments across its merchant base; Coinbase launched x402; JPMorgan launched a deposit token, JPMD; SG-FORGE issued a stablecoin; Fiserv launched FIUSD

July 2025: Goldman Sachs and BNY Mellon launched tokenized money market fund

September 2025: HSBC expanded its tokenized deposit service (TDS); CFTC greenlighted stablecoins for derivatives; Stripe launched Tempo

October 2025: Mastercard reportedly entered discussions to acquire ZeroHash for up to $2B; Zelle and Western Union integrated stablecoins; Ant Group launched Jovay Network; Circle launched Arc

November 2025: BNY Mellon launched stablecoin‑reserves fund; Circle released xReserve; Japan’s first stablecoin was launched

December 2025: A consortium of 10 European banks, including BNP Paribas and ING, formed a dedicated company to launch a euro‑pegged stablecoin; Stripe incubated Tempo.

January 2026: Tether launched USAT; Fidelity launched FIDD stablecoin; Polygon pivoted to payments

February 2026: MoonPay partnered with Deel on stablecoin payroll; Anchorage Digital launched a stablecoin solution; Citi picked Solana for stable‑value PoC

Within months, Amazon and Walmart began exploring stablecoins. Visa and Mastercard have both rolled out products that let users spend stablecoins through traditional payment networks, while platforms like MetaMask, Kraken, and Crypto.com now offer card-linked stablecoin spending for everyday purchases.

The pattern is unmistakable: institutional FOMO at scale.

The Infrastructure Pain Point

Why the sudden urgency? Because traditional financial rails are inadequate for modern business.

Cross-border payments remain slow and expensive. Wires pass through correspondent banks. Settlement can take days. FX spreads and fixed fees accumulate. For firms operating across emerging markets, the friction is greater still.

Stablecoins compress clearing and settlement into a single on-chain transaction. They settle quickly and at lower marginal cost. For treasury teams managing liquidity across subsidiaries, that is a practical improvement.

Yet stablecoins do not remove banks from the equation. Fiat still requires entry and exit points. Compliance still applies. Liquidity must be monitored across currencies and chains. The blockchain may be public, but the operational layer is not.

As Max puts it: “Stablecoins are the better rail - instant, programmable global settlement. But what always breaks is fiat connectivity. That’s where the real work is.”

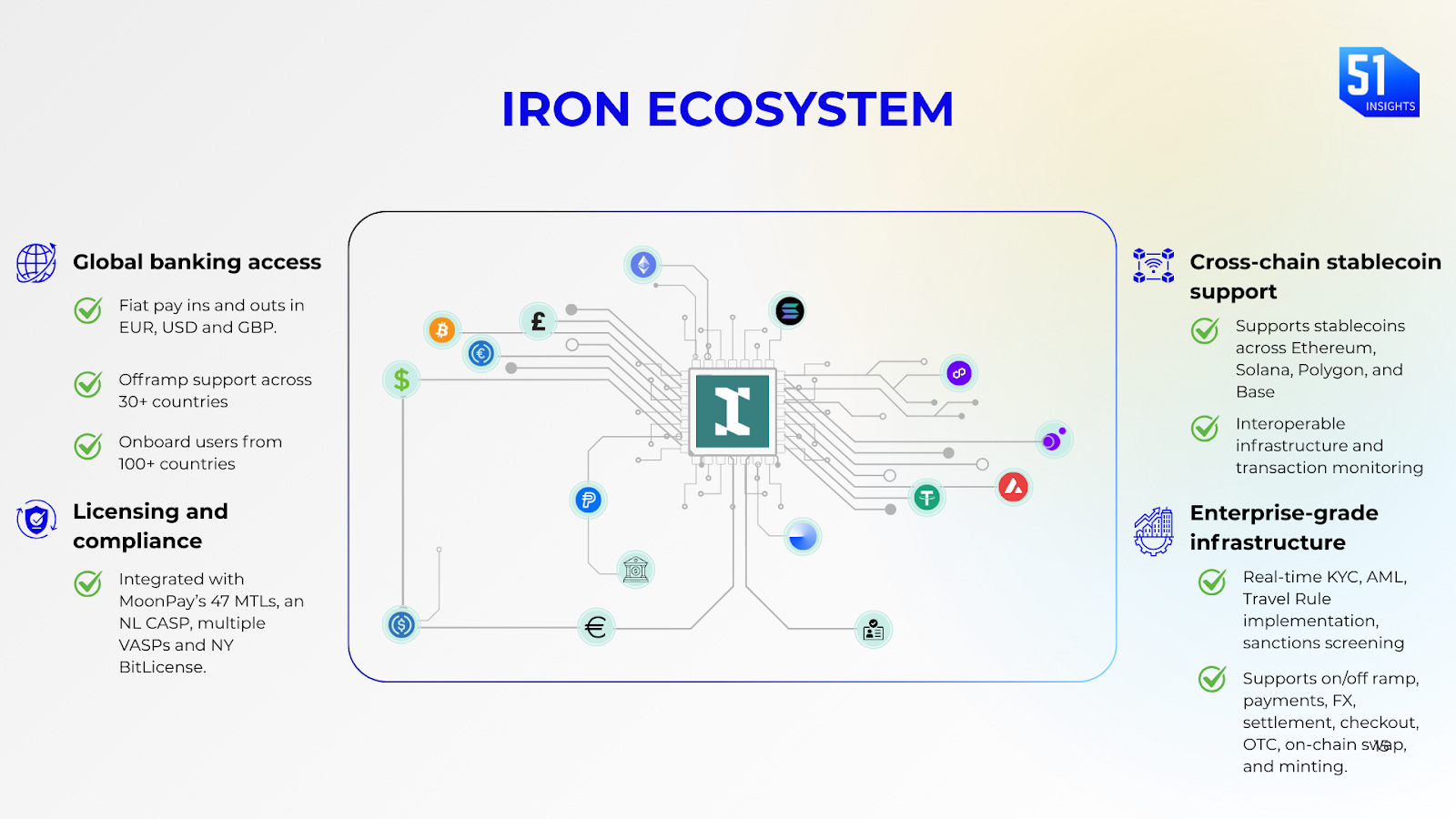

Infrastructure, Not Just Tokens

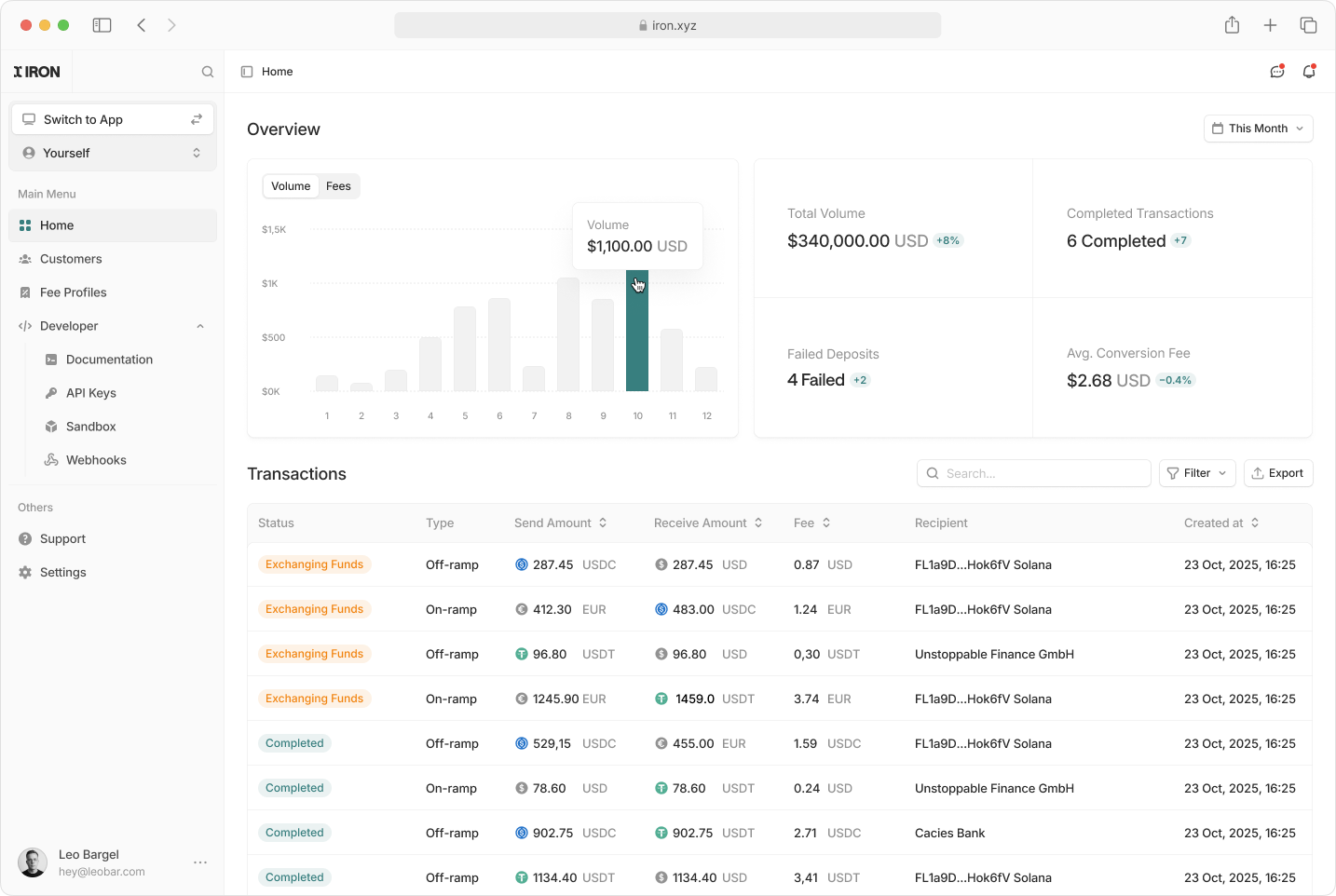

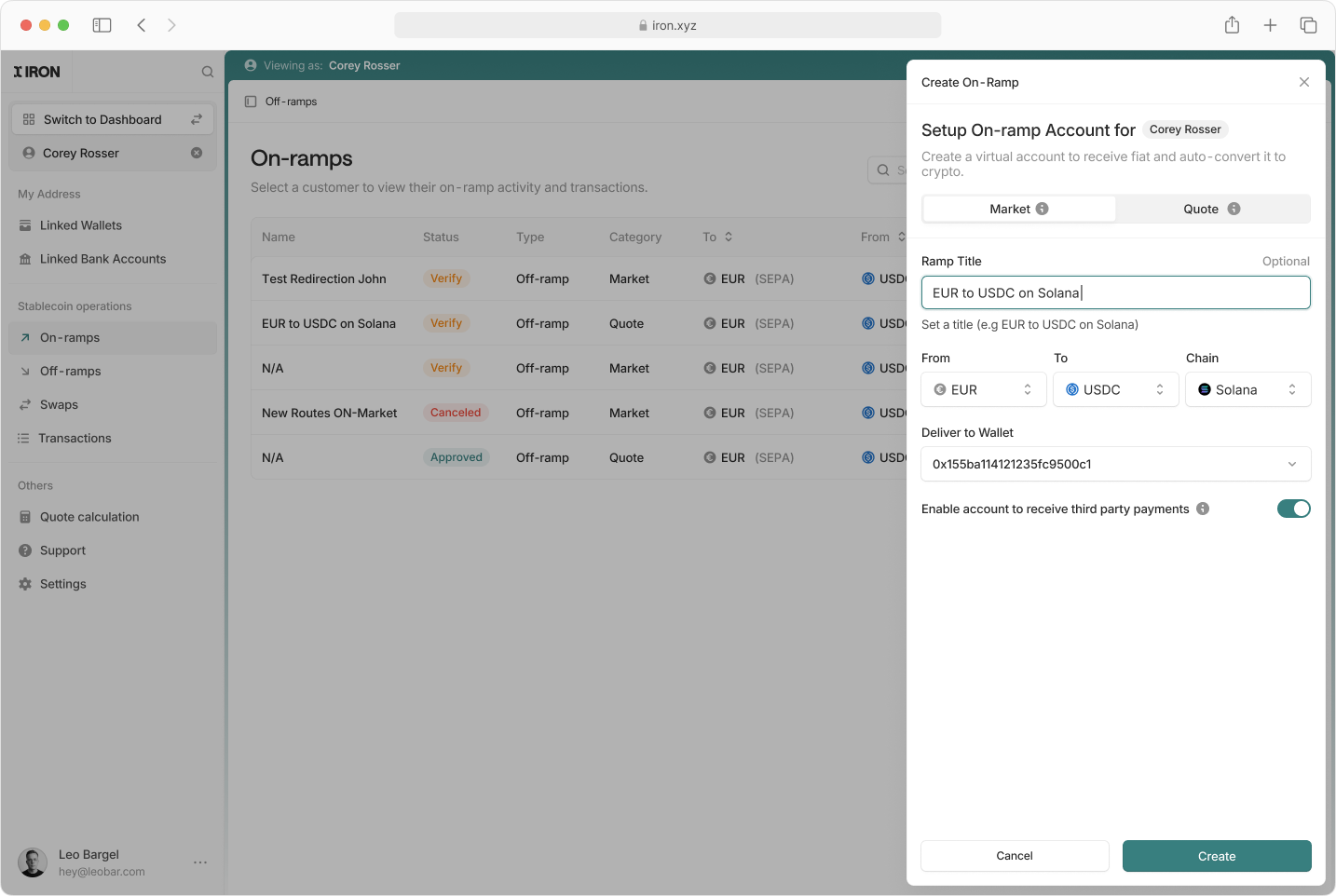

Iron focuses on that connective layer. It provides APIs that allow fintechs and enterprises to move between fiat and stablecoins. It offers cross-border payouts, multi-chain settlement and named virtual accounts - where incoming funds are immediately auto-minted to local currency stablecoins and delivered to users’ self custodial wallets linked to Iron.

Behind a single integration sit multiple bank relationships, licences and blockchain connections. A company can wire euros to a dedicated IBAN and receive stablecoins shortly after. It can send stablecoins and have funds arrive in a local bank account via networks such as SEPA or PIX.

Iron also supports custom stablecoin issuance in partnership with the M0 protocol. Clients can launch branded, fully reserved stablecoins with embedded compliance logic. Iron manages minting, redemption and fiat rails. Issuance becomes part of the same infrastructure stack.

The complexity is largely invisible. Each jurisdiction has distinct regulatory demands. Each bank integration behaves differently. Each blockchain has separate mechanics. Enterprises expect this to function as a unified system.

“We had to build one API that works across multiple banks and payment providers,” says Max. “You don’t realise how hard that is until you try to make it homogeneous, fast and reliable.”

MoonPay’s acquisition reflects that logic.

For years, MoonPay was synonymous with card-based crypto access. But cards don’t scale for enterprise. And enterprises don’t just need access, they need infrastructure: banking, compliance, liquidity, and local payout rails. MoonPay saw the opportunity for Iron to fill that gap.

By adding Iron’s rails and issuance capabilities, MoonPay moves from access to infrastructure.

The B2B Unlock

The killer use case for stablecoins is B2B payments.

Global corporations move nearly $23.5 trillion across countries annually, equivalent to about 25% of global GDP, resulting in $120B transaction costs per year.

Payroll provides a clear example. In 2026, MoonPay partnered with Deel to enable stablecoin payouts. Employers remain fiat-based. Workers can opt into stablecoins. Conversion, compliance and settlement are handled in the background.

Companies are more concerned with certainty than with blockchains. They want regulatory coverage, counterparty stability and operational resilience. Stablecoin infrastructure providers compete on those dimensions.

Max is explicit about the direction of travel: “Pretty much every fintech in the next 24 months will have stablecoin support. You simply can’t compete globally without it.”

Today’s Stablecoin Landscape

The market is moving fast, and the major players are each staking out territory. Stripe, through its acquisition of Bridge and the launch of Tempo, is extending its merchant reach into crypto-native settlement. Circle is focused on issuance and the USDC ecosystem. BVNK is building enterprise orchestration tooling. And the large banks are developing token systems, though often within closed, proprietary networks.

Each solves a piece of the puzzle. But for enterprises looking to move on stablecoins, stitching together point solutions across issuance, compliance, on-ramps, settlement, and distribution means managing multiple vendors, multiple integrations, and multiple points of failure.

That’s the gap MoonPay fills.

MoonPay doesn’t do one thing best, it does everything an enterprise needs in a single stack. Consumer ramps, merchant settlement, custom stablecoin issuance, regulatory infrastructure, and deep connectivity into DeFi and crypto-native ecosystems all sit within one architecture. That means:

Distribution: embedded across wallets, apps, and platforms with 35M+ consumers already transacting

Regulatory infrastructure: extensive U.S. Money Transmitter Licenses, a New York BitLicense, a Limited Purpose New York Trust Charter and MiCA licensing in Europe

Issuance: a custom stablecoin issuance stack, including integration with M0

Agentic payments: An emerging design for AI-driven and autonomous transactions

MoonPay’s strategy is vertical integration. Consumer access, enterprise rails, issuance tooling and DeFi connectivity sit within one architecture. Few competitors offer that combination in a single stack.

EY reports that 13% of financial institutions and corporates globally currently utilize stablecoins, and 54% of non-users expect to adopt stablecoins within 6-12 months.

The question isn’t whether this will happen. The question is who will own the infrastructure when it does.

The Next Fintech Stack Will Be Stablecoin-Native

Today’s Fintechs face brutal expansion constraints.

Expanding from Europe to Latin America means negotiating new banking partners, navigating local compliance, and building country-specific payment rails. Each new region can take 12-18 months to activate.

And cross-border payments? Still stuck with 3-7% fees and multi-day wire transfers.

Max saw this problem everywhere: “What’s the glue to the traditional world?” he asks. “It always breaks at fiat connectivity.”

Stablecoins flip the model.

Instead of building relationships market-by-market, fintechs can plug into one API and unlock global coverage instantly.

The Market Is Already Moving

Max sees the demand daily: “More and more fintechs like the Nubanks of the world, even Revolut, are starting to build on top of stablecoins because you can build global payment and banking experiences on top.”

These aren’t crypto companies. They’re traditional fintechs and enterprises choosing stablecoins because the economics are undeniable.

71% of Latin American businesses and 43% of B2B transactions in Southeast Asia now use stablecoins for cross-border payments.

Globally, stablecoins accounted for about 30% of all on-chain crypto transaction volume in 2025, reaching over $4 trillion in annual transaction volume by August 2025, an 83% increase year-over-year.

The Stablecoin Endgame

Stablecoins are the new rails of money movement.

If stablecoins become embedded in finance, they will fade into the background. Users will not think about blockchains. They will send and receive money.

The shift will be gradual: Banks will remain central and payment networks will endure, but parts of cross-border settlement, treasury management and even private issuance may migrate to tokenized fiat.

In that world, value accrues to those who connect digital tokens to the traditional system - and who enable others to issue their own. Stablecoins alone are not the moat. Infrastructure is.

MoonPay’s purchase of Iron is a wager on that premise. The tokens may be stable. The contest around them is not.

That’s it for now.

Take care,

Marc

PS: Follow me on LinkedIn and X for shorter insights.

This article is published in collaboration with MoonPay. As the authors, I maintain full editorial integrity and the views and insights expressed are my own, ensuring the content remains unbiased and authentic.

🚨 Want more intelligence? Work with the 51 Intel team to embed continuous, high-signal market intelligence into your organization.