12 signals the ambiguity is over

Today we’re publishing our 2026 Outlook: The End of Crypto Ambiguity

Hey, it’s Marc & 51 team,

For the last decade, the primary risk in digital assets was moving too early. Allocating to unproven technology. Navigating reputational exposure. That calculus just flipped. In 2025, the risk became inaction.

And here's the data that proves it.

Today we’re publishing our 2026 Outlook. It covers

12 signals from 2025 that rewired the market

8 structural patterns reshaping how capital moves

Our top predictions for what breaks through in 2026

The institutional reports worth your time

What actually happened in 2025

After ten years in crypto, 2025 was the first time I could say it with complete conviction: it’s actually different this time.

I know, dangerous words. But hear me out, because I’m not talking about price. Or retail hype. I’m talking about plumbing. This is Fortune 500 companies and trillion-dollar banks rebuilding their financial stack on blockchains into real systems: custody, collateral, settlement, tokenized cash, tokenized Treasuries.

Every major US bank is now upgrading its infrastructure. The biggest payment companies are integrating blockchain. Stablecoins turned into a geopolitical weapon for “dollarization”, and Bitcoin became a geopolitically relevant asset.

Which brings me to the question that’s been rattling around in my head since October: Are we in for a prolonged four-year cycle? Or are we about to enter a bear market? And what do executives need to focus on now?

In 2025, the world’s largest financial institutions stopped testing blockchain technology and started depending on it. This changes nearly everything about how capital will move, who captures value, and where the real opportunities sit heading into 2026.

Three developments stood out:

1. Regulatory clarity

2025 delivered something crypto has never had before. Regulatory certainty. The GENIUS Act passed on July 18th, the first federal framework for payment stablecoins. The OCC approved five national trust bank charters for digital asset companies, including Circle and Ripple.

2. A maturing infrastructure layer

The DTCC, the company that processes nearly every stock trade in America, received regulatory clearance to tokenise U.S. assets, including Treasury bonds and ETFs. SWIFT, the 50-year-old network that moves roughly $5T in payments every day, partnered with more than 30 global banks to build real-time settlement on Ethereum. These are not experiments. They are the replacement of legacy plumbing.

3. The distribution floodgates opened

Bank of America authorised its advisors to recommend digital asset allocations to approximately 70M clients. Vanguard, which spent years refusing to offer any crypto exposure, quietly reversed course. JPMorgan began accepting Bitcoin and Ethereum as loan collateral, alongside gold and U.S. Treasuries. These are the institutions that manage retirement savings, college funds, and pension assets for ordinary Americans. When they move, capital follows at scale.

🚀 A lot more is going on that we’ll tell you in our PRO briefings.

If you’re an institutional professional making decisions in this space, you’re flying blind without PRO. 35k+ executives read us every single week.And they don’t just skim headlines — they use our intelligence to make actual decisions.

The pattern beyond the headlines

The early narrative around blockchain was fundamentally adversarial, technology built to circumvent banks, remove intermediaries, and return control to individuals. That narrative produced genuine innovation and also a decade of regulatory friction. What happened in 2025 is that the largest incumbents decided the technology was too useful to fight and too consequential to ignore.

JPMorgan now runs its own digital deposit token. A consortium including Citi, Wells Fargo, and PNC is building a shared digital currency for payments. Goldman Sachs expanded crypto lending. BNY Mellon and Citi scaled custody operations. Morgan Stanley plans to offer crypto trading through E-TRADE in the first half of 2026.

The strategic logic: whoever controls the settlement layer, the custody infrastructure, and the payment rails captures a toll on every transaction. Banks understand this better than anyone. They built those moats over decades in traditional finance. They are now rebuilding them in the new architecture, and this time, they are doing it on public blockchains.

Want more intelligence? Work with the 51 Intel team to embed continuous, high-signal market intelligence into your organization.

Three numbers you need to know:

$33T — Stablecoin transaction volume in 2025, up 72% year-over-year. That rivals Visa’s global network. The stablecoin market now exceeds $300B in total value. Stablecoin issuers are the 7th largest purchaser of U.S. government debt. Washington didn’t regulate stablecoins because it feared them. It regulated them because they fund the deficit.

$40B+ — Total tokenized real-world assets, up roughly 8x since 2022. BlackRock’s tokenized Treasury fund exceeded $2.5B in AUM. More than half the world’s twenty largest asset managers launched or planned tokenized products. BCG and Ripple project this market hitting $18.9T by 2033.

$37B — Record crypto M&A in 2025, 7x the prior year. These weren’t fire sales. Coinbase paid $2.9B for Deribit. Kraken paid $1.5B for NinjaTrader. Mastercard is acquiring stablecoin firm ZeroHash. Buyers paid full price for one thing: speed-to-market. The acquisition window for established positions is closing.

Our top 5 predictions from the report

The full-stack takeover accelerates. Exchanges, custodians, and wallets will continue merging into single platforms that control the entire customer journey: issuance, trading, custody, and payments. Banks will acquire crypto companies specifically for their stablecoin and compliance capabilities, not their technology. Crypto-as-a-service infrastructure will capture market share faster than any bank can build internally. The race isn’t over who has the best product. It’s over who owns the pipes.

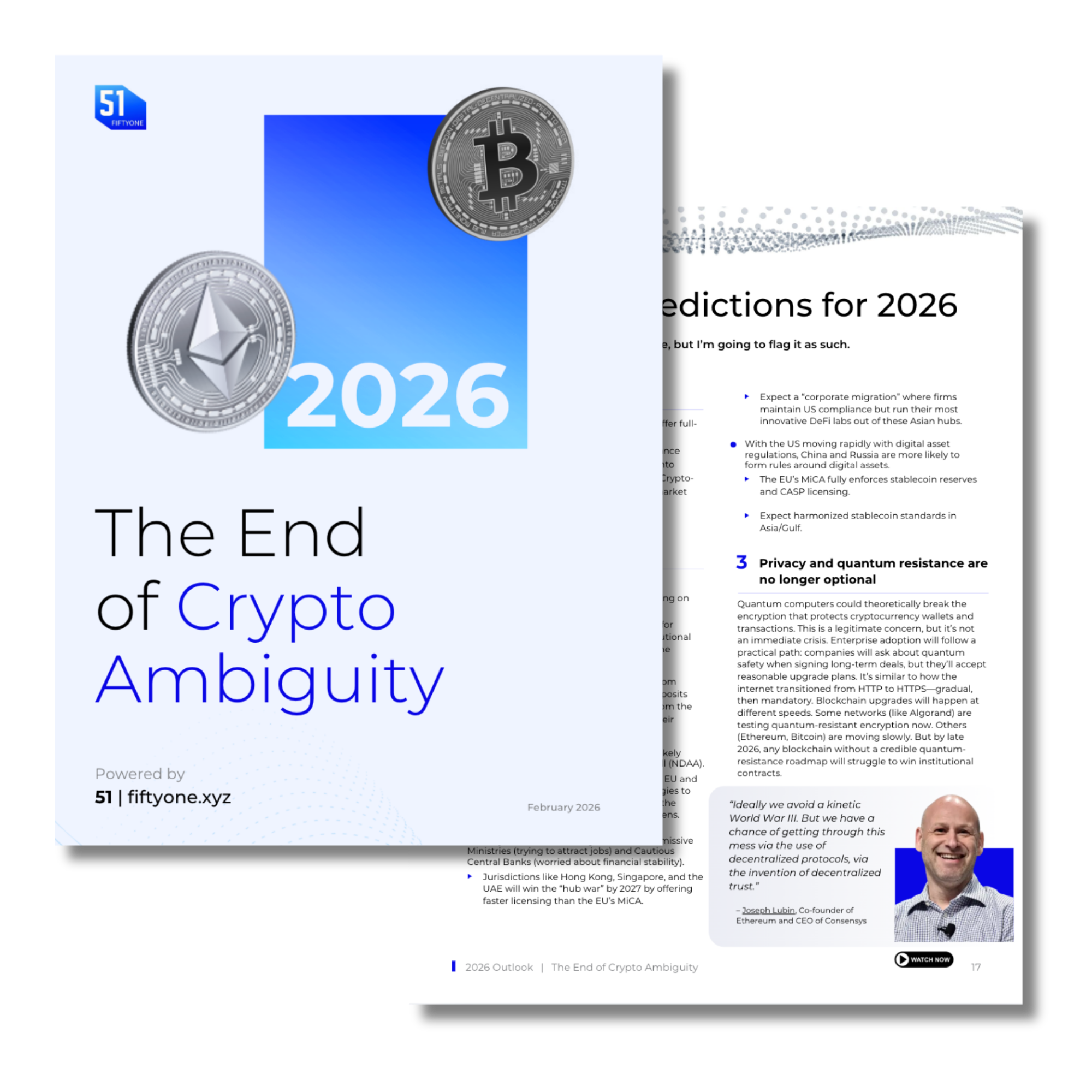

24/7 settlement becomes the baseline, not a premium. Any B2B payment platform that can’t process a transaction on a Saturday will be considered legacy infrastructure by Q3 2026. Worldpay’s round-the-clock USDC settlement on Solana has already forced the question. JPMorgan and Citi will respond by making 24/7 settlement a standard offer. The turning point will be a Fortune 100 treasurer publicly stating they walked away from a banking relationship because of weekend settlement limitations. That moment is coming.

Prediction markets reach $50B in notional volume. Polymarket will either IPO or get acquired by a regulated exchange. Kalshi, CME, or Nasdaq are the most likely buyers, after demonstrating sustained quarterly volume above $10 billion. The more interesting development is what the volume will be used for: corporate earnings hedges, studio box office risk, political campaign positioning. Accusations of manipulation will follow. Someone will face legal consequences. Vitalik highlighted structural issues. The category will grow regardless.

AI agents take control of $10B in DeFi capital. Autonomous software agents will manage more capital in decentralized finance than the top 50 individual crypto holders combined by Q4 2026. They will handle yield optimization, portfolio rebalancing, and liquidity provision as standard functions. The risk is real: a rogue agent will cause a nine-figure exploit, creating the first major AI liability legal case. Courts will not be prepared for it.

For the first time, token fundamentals actually matter. 2026 will be the first cycle where revenue-generating protocols outperform governance tokens and memecoins on a risk-adjusted basis. The structural mispricing is already visible: applications generate roughly 70% of total crypto sector revenue but account for only 7% of market value. As institutional capital learns to apply standard software valuation frameworks, revenue multiples, margin analysis, and competitive moats, that gap closes. Protocols with real cash flows will trade on fundamentals. If you are still allocating based on narratives, you are positioned for the last cycle, not this one.

The financial system is being rebuilt on blockchain. The regulatory framework supports it. The capital allocation decisions that follow will be massive.

But here’s what most people miss: the biggest value won’t go to the infrastructure layer. It’ll go to whoever builds applications that own lasting customer relationships on top of it.

If you’re still waiting for proof – it shipped in 2025.

Take care,

Marc & team

🚨 Want more intelligence? Work with the 51 Intel team to embed continuous, high-signal market intelligence into your organization.

This briefing is based on the FiftyOne 2026 Outlook: The End of Crypto Ambiguity. The full report covers 12 market signals, 8 structural patterns, institutional adoption data, and specific predictions for 2026. Nothing here constitutes investment advice.

stablecoin issuers are the 7th largest buyer of US debt. no wonder congress moved so fast on the GENIUS Act lol. maybe CLARITY act incoming soon