Money Movement 2.0: 2026 Edition [Report]

Today, live from Proof of Talk in Paris, we are publishing Money Movement 2.0 (2026), our most rigorous stablecoin report yet.

Hey, it’s Marc. A year ago we wrote that money was moving, and that this time it was real. Stablecoin supply was $250 billion with monthly settlement of $2.3 trillion.

The frame was: this is real, and it is accelerating.

We underestimated the speed.

Supply just crossed $323 billion. In March 2026, stablecoins settled $7.5 trillion in a single month, surpassing the U.S. ACH network for the first time in history. Tether and Circle, between them, now hold more U.S. Treasury bills than Germany. The GENIUS Act is law. The CLARITY Act is on deck. Three of the five largest American banks have publicly confirmed they are exploring stablecoin issuance, and BlackRock, Morgan Stanley, and Franklin Templeton are racing each other to manage the reserves behind them.

That is not adoption. That is a phase change.

Today, live from Proof of Talk in Paris, we are publishing Money Movement 2.0 (2026), our most rigorous stablecoin report yet. The first edition documented adoption. This one documents the infrastructure being built on top of it, and the people who will own the rails when the dust settles.

What’s In The Full Report

State of play. The biggest monetary realignment in 50 years. Why $323B in supply matters beyond crypto.

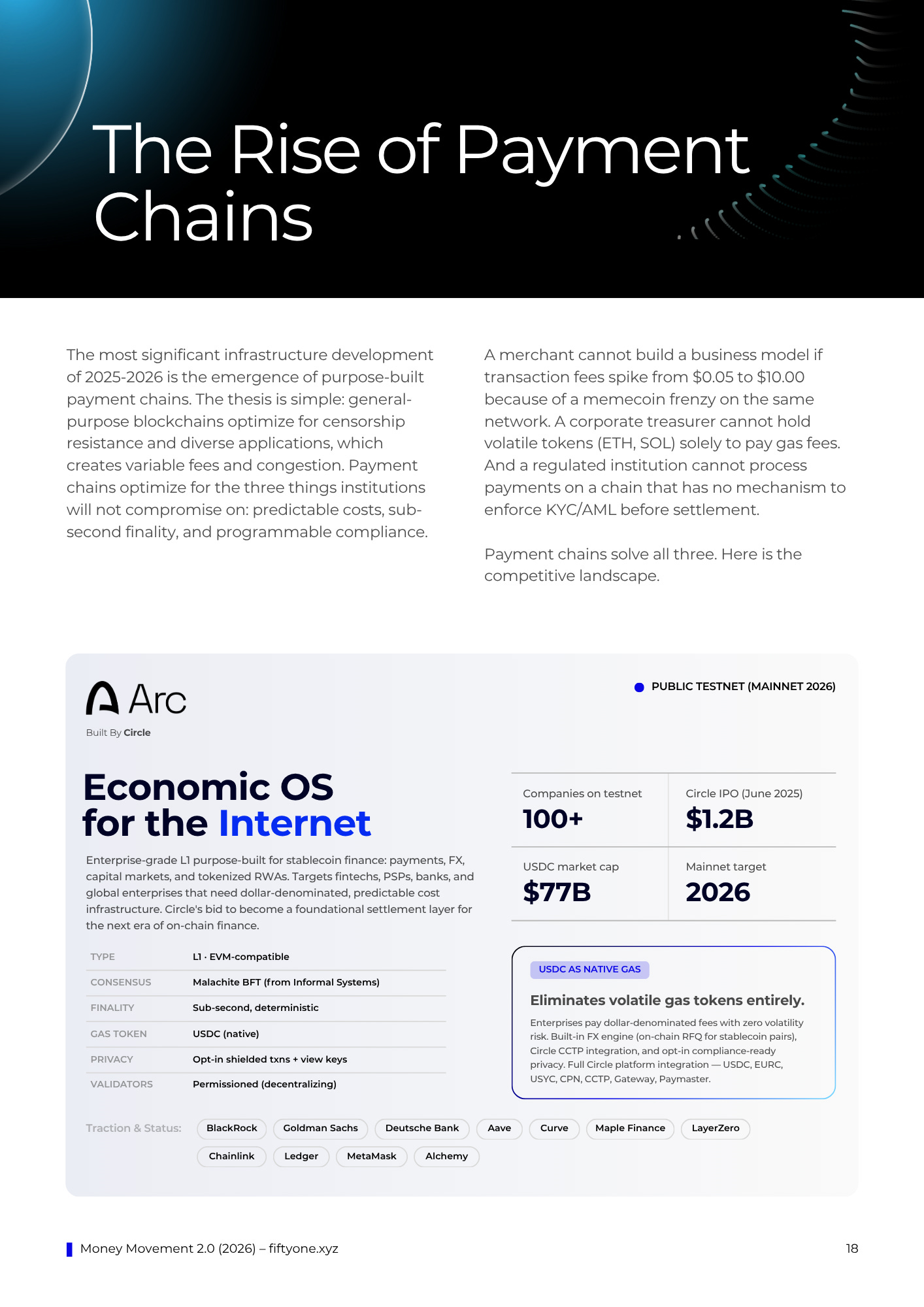

The rise of payment chains. Arc, Tempo, Plasma, Stable, Canton, ZRO, Avalanche subnets, the L2 “door” architecture.

The interoperability stack. CCTP, LayerZero, Wormhole, Axelar, and SWIFT’s interlinking pilot with BNP Paribas, Intesa Sanpaolo and Société Générale.

The institutional trust architecture. Attestation vs. audit, AICPA AT-C 205, Tether’s KPMG audit, the four-layer stack.

Top 7 use cases. Treasury demand, tokenized collateral, wholesale settlement, B2B/cross-border, capital markets, EM remittances, machine-tomachine payments.

Institutional case studies. BlackRock (BUIDL), JPMorgan (Kinexys), Goldman Sachs (Canton/GS DAP).

The regulatory map. GENIUS Act, MiCA, Hong Kong, Singapore, Japan, UAE, Brazil, India, Nigeria.

What’s next. The synthetic CBDC, T+0 settlement, the two-sphere stablecoin world, and the M&A wave that has not peaked.

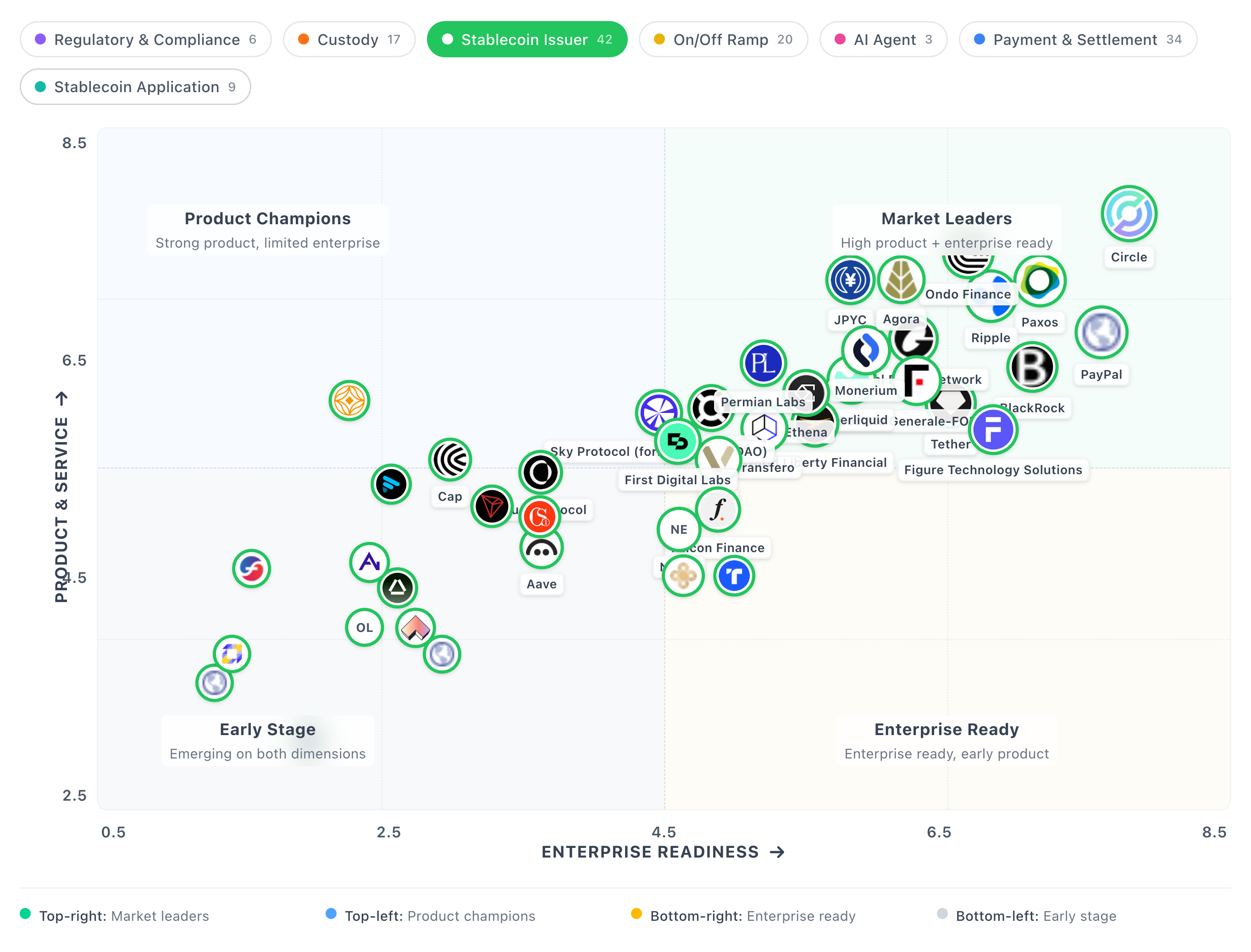

Bonus: 2,000+ vendor database with 51 Trust Scores across stablecoin issuers, payment chains, wallets, custody, on/off ramps, AI-agent settlement.

🚀 Build credibility. Drive pipeline. Win in digital assets. We produce institutional-grade research that positions you as the authority in your category, then distribute it to 100,000+ decision-makers who act on what we publish.

How are Stablecoins Rewiring Global Finance?

If you read a stablecoin report two years ago, the question was whether they would survive. In 2026 the question is who controls the rails they run on.

What happened: ACH, the workhorse of American payments since 1972, was passed in monthly volume by a system that did not have a federal legal framework twelve months ago. Stripe paid $1.1 billion for Bridge. Mastercard paid $1.8 billion for BVNK, the largest stablecoin M&A deal in history. Visa quietly took its stablecoin settlement program from a pilot to a $7 billion annualized run rate. Western Union, which spent two centuries moving paper across borders, launched a stablecoin in May on Solana.

You can argue with the gross number. A lot of the $7.5 trillion is wholesale, DeFi, and bots. Real-world payment volume, stripped of trading and automated treasury sweeps, is closer to $400 billion a year. That sounds smaller, until you remember it is growing at 90% year-on-year off a base that did not exist three years ago.

The honest version: a parallel financial system is being laid down in production, in plain sight.

“Stablecoins are essential to transacting on blockchain rails. Using stablecoins will make it feasible for broker-dealers to engage in a broader range of business activities.”

— SEC Commissioner Hester Peirce

Stablecoin issuers quietly became sovereign creditors

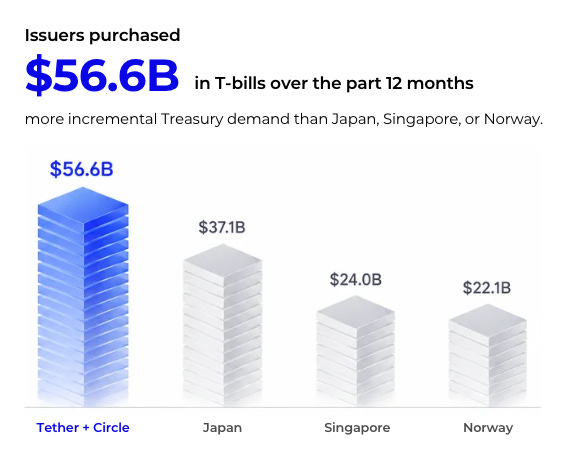

Tether holds $122 billion in direct U.S. Treasury exposure. Add repos and the number is $141 billion. Circle's USDC reserves, managed by BlackRock inside the Circle Reserve Fund, hold another $30 to 40 billion of T-bills and overnight repos. Together they bought $56.6 billion in T-bills last year, a bigger source of incremental Treasury demand than Japan, Singapore, or Norway.

Standard Chartered projects $1 trillion of net-new T-bill demand from stablecoins by 2028.

This is the thing the GENIUS Act actually fixed. It mandated 100% reserves in cash, Fed balances, or short Treasuries. It clarified that 1:1 backed dollar coins are not securities. It made the issuer a kind of narrow bank, sitting on T-bills on one side and demand-redeemable dollars on the other, supervised at the federal level.

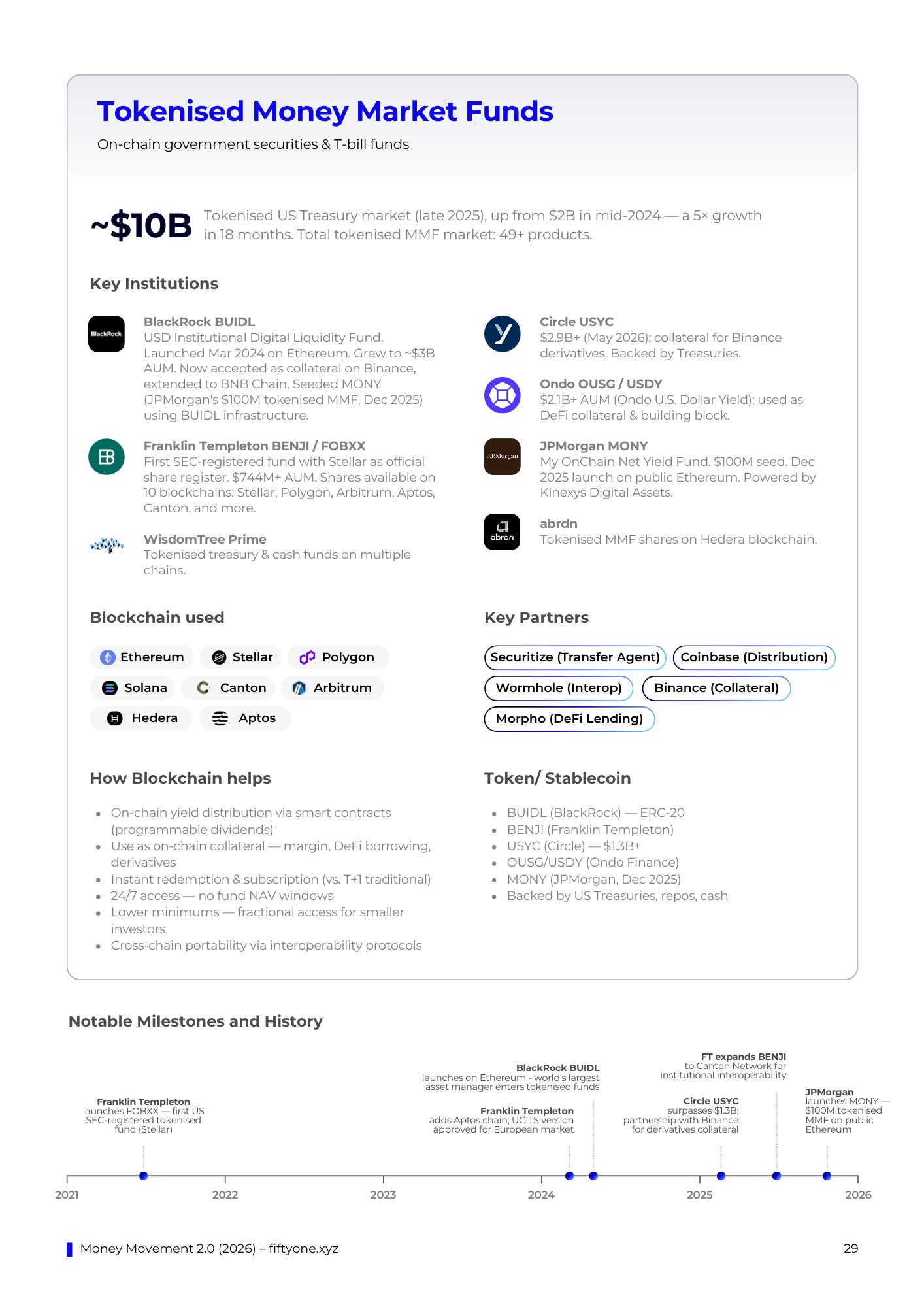

Tokenized cash ate idle dollars

Tokenized money market funds went from $100 million in early 2024 to over $20 billion by May 2026. That is 150x in two years.

BlackRock's BUIDL is now accepted as Binance margin collateral. Translation: an institutional trader can earn ~3.4% on T-bills and simultaneously post that yieldbearing dollar as exchange margin. Before this existed, the same trader held USDT and ate the opportunity cost. Now they do not have to.

In May 2026, BlackRock filed for BRSRV (Daily Reinvestment Stablecoin Reserve Vehicle), a tokenized fund purpose-built to sit underneath stablecoin reserves. Morgan Stanley launched MSNXX, its Stablecoin Reserves Portfolio. JPMorgan launched MONY in December. SIFMA recommended classifying these things as cash equivalents under U.S. GAAP.

The 4% T-bill yield is no longer trapped in the issuer's P&L. That is a trillion-dollar incentive that just got unlocked.

🚨 The PRO terminal is launching soon. This means: real time intelligence on digital assets news flow, 2000+ digital asset vendors tracked with deep product data and our proprietary vendor ratings (like Gartner, but 10x better), 10+ sector maps, intelligent signal feed and a co-pilot that’s trained on all our data. 👉 Secure your spot on the waitlist & secure access to our beta.

Payment chains, or the part that is actually new

General-purpose blockchains were never designed to move money. They were designed to be uncensored and diverse, which is the opposite of what a global payments network needs. A merchant cannot run a business on a network where gas fees spike from $0.05 to $10 because someone minted an NFT. A corporate treasurer cannot hold ETH to pay gas, because every fee triggers a capital gain. So a category of purpose-built payment chains was born.

We have dissected the top chains in the report.

The future of payments is agentic

Today, 70 to 90% of stablecoin volume is already programmatic. Bots, market makers, algorithmic arbitrage, automated treasury sweeps. So when people ask whether AI agents will need stablecoins, the answer is they already use them. We just call those agents "trading systems."

What changed is standardization. Coinbase's x402 protocol turns the HTTP 402 "Payment Required" error code into a primitive. An agent calls an API, receives a 402, resolves it with a micropayment, and gets the data. 69,000 active agents and 165 million transactions as of April 2026. Visa Intelligent Commerce has 100+ partners and 20+ live agent integrations. Mastercard Agent Pay shipped. Amazon Bedrock AgentCore Payments went live in production, co-built with Coinbase and Stripe.

The reason traditional payment rails cannot serve agents is structural. Cards settle in three to five days. Cross-border requires currency conversion. Every authorization assumes a human. Subscriptions assume monthly billing. Agents need none of those things. They need internet-speed money that works at the cent level, 24/7, with no human in the loop.

That is what stablecoins are. Internet money for internet-speed commerce

Who's winning

The dust is settling. Incumbents are building to own the plumbing. Banks are talking the path of tokenised RWAs to handle collateral and distribution. Whereas, some crypto-native platforns are leading while some are getting acquired by traditional leaders.

We have also gave a sneak peak of our institutional vendor intelligence platform covering 2,000+ vendors across stablecoins and tokenization in the report.

Circle and Stripe aren't improving SWIFT, they're building around it. Every year the parallel infrastructure gets more capable, cheaper, and better regulated. Every year the cost of ignoring it goes up.

The companies that move first on stablecoin integration will gain two things: direct cost savings (often 60–90% on applicable payment flows) and supplier network lock-in. Once your suppliers accept stablecoin payments and benefit from instant settlement, switching back to wire transfers looks like a downgrade.

The companies that wait will face margin compression as early movers reduce their cost structures and use the savings to undercut on price.

Central banks see this clearly, which is why European banks are launching a stablecoin even after the ECB president warned about stablecoins “privatizing money.”

Take care,

Marc