Hey, it’s Marc,

I keep asking bank executives the same question: when does an AI agent make its first real purchase inside your system?

On March 2, Santander answered it. An AI agent completed a live, end-to-end payment on real rails, no human at checkout. The $5 trillion checkout just got its first non-human customer. [RELEASE]

Let’s unpack.

👉PRO: Download the PDF at the bottom

What happened

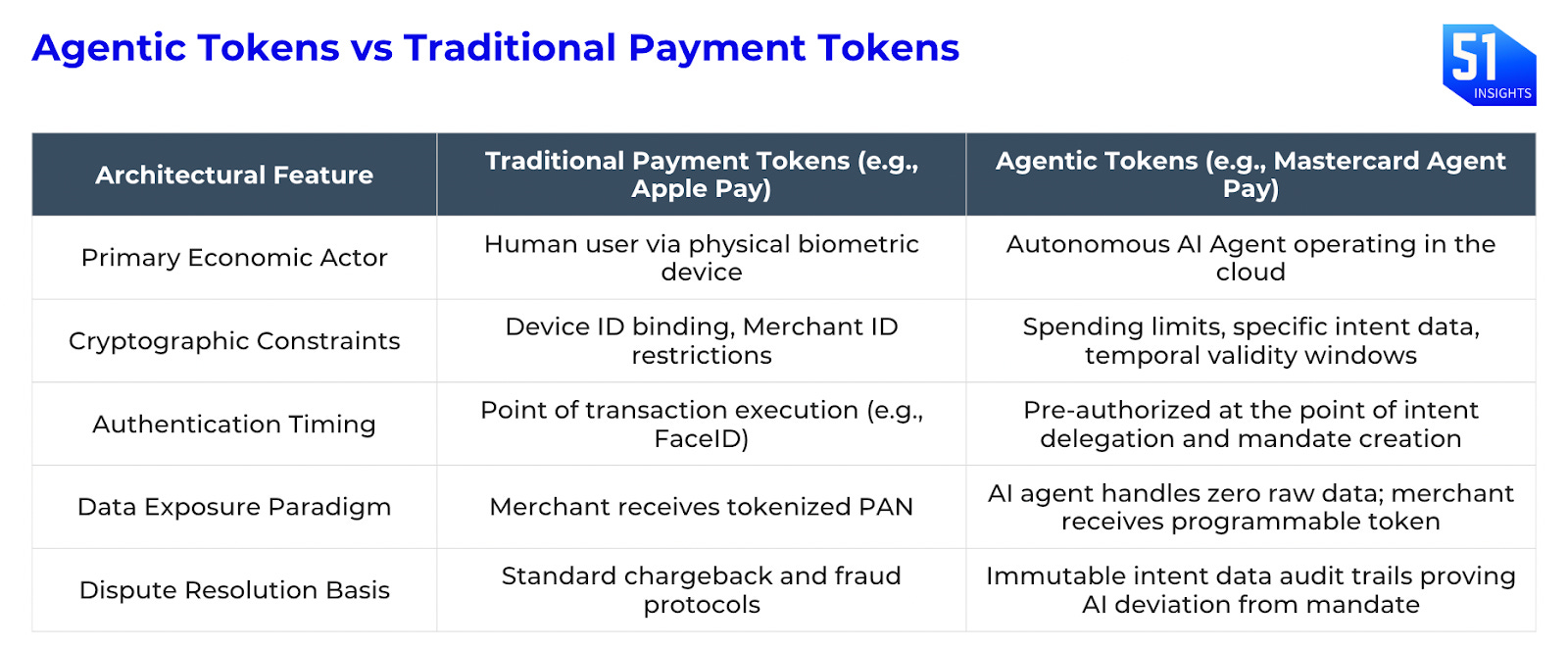

Santander and Mastercard executed Europe’s first live AI-agent payment using two integrated systems: Mastercard’s Agent Pay protocol and PayOS, a billing platform that converts vaulted credentials into PCI-exempt proxy cards.

The AI agent accessed no raw financial data. It transacted entirely within a cryptographic “mandate,”pre-authorized by the user with hard limits on what it could spend, where, and when.

The transaction ran through Santander’s normal payments network, validating the full operational and control framework under real-world conditions.

In short: The $5 trillion checkout is being rewritten for machines.

Santander is not alone: DBS in Singapore (one pilot under Visa Intelligent Commerce (VIC), while another with Mastercard and UOB), and Commonwealth Bank of Australia have already piloted similar capabilities using Visa and Mastercard frameworks.

Zooming in: Mastercard’s AI models are trained on over 160B annual transactions to enhance security, detect fraud, and enable new technologies such as Agentic Commerce.

But, data is not enough. An agentic model payment also requires an entirely new trust architecture.

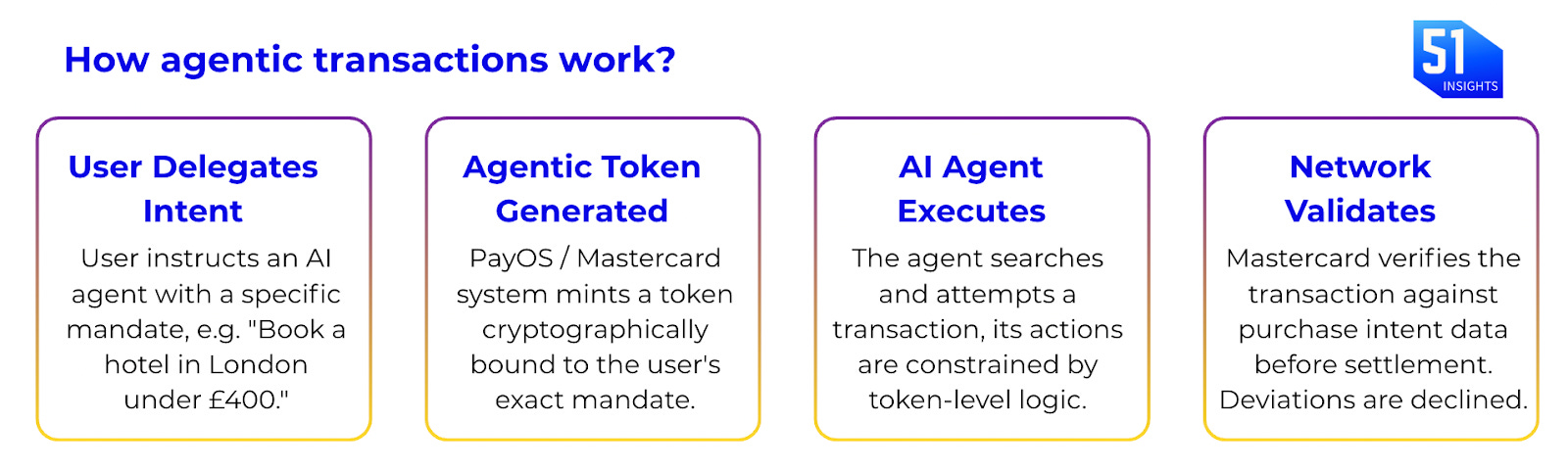

Here is how it works: The agentic system has 3 layer trust architecture moving from user to token to network. AI agent acts within its authorized scope, whereas, merchant category aligns with the mandate.

Another example: A user tells their AI travel agent: “Book me a flight to London, economy class, under £350.” An Agentic Token is created encoding this exact intent. If the LLM hallucinates and attempts to book a business class ticket at £780, the transaction is categorically declined at the network level, before any money moves. The intent data audit trail is preserved for any dispute resolution.

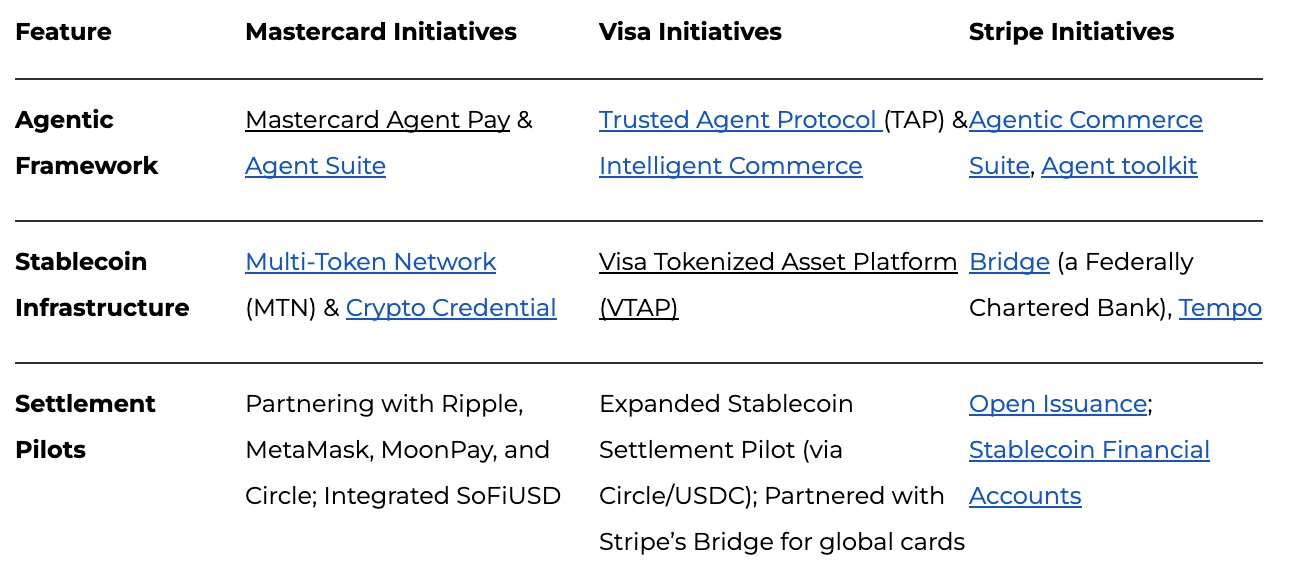

Mastercard vs Visa: Agentic payments and stablecoin initiatives at Mastercard and Visa are converging to create a “trust layer” for autonomous AI commerce. They are building for AI to handle the decision making while blockchain provides the programmable settlement.

Table 2: Mastercard vs Visa vs Stripe

Zooming out: The scale of agentic commerce shift is staggering. Morgan Stanley models that U.S. e-commerce spending initiated by AI agents will reach $190B to $385B by 2030. McKinsey projects global agentic volume could hit $3T to $5T in the same window. The transition from “search, filter, scroll” to instant, API-driven intent execution is happening right now.