US Banks are going on-chain

JPMorgan, Citi, BofA, and Wells Fargo just announced a shared tokenized deposit network through The Clearing House, targeting 2027. Here's what it means for stablecoins and enterprise payments.

Banks spent a year lobbying against stablecoin yield. Last week they stopped arguing and started building. JPMorgan, Citi, BofA, Wells Fargo, and 13 more banks just announced a shared tokenized deposit network through The Clearing House, targeting an H1 2027 launch. It’s Wall Street’s most coordinated answer to stablecoins yet: a response to the CLARITY Act’s yield fight and a deposit-flight scenario worth $3.7T in destroyed deposits. [NEWS] [RELEASE]

The Signal: Tokenized deposits won’t erase stablecoins. But they will push them out of enterprise B2B rails. JPMorgan already runs JPMD. HSBC, Citi, and BNY are building theirs. Expect three layers to co-exist: bank consortium tokens for wholesale settlement, regional networks like Cari for the mid-market, and USDC and USDT for permissionless global commerce, remittances, and DeFi.

👉 PDF for PRO readers at the bottom

🚨 Vendor diligence in digital assets takes 2-3 weeks of primary research. 51 Terminal does it in an afternoon.

2,000+ vendors. Up to 95 data points per company. The 51 Trust Score: the only quantified, defensible vendor rating in digital assets. Plus sector maps, an impact-scored signal feed, and an AI copilot trained on the full dataset.

Built for consulting teams, corporate strategy, and allocators. Early users report 2-5x faster diligence.

We’re opening 25 founding accounts before public launch. Founding members lock launch pricing and get direct input on the roadmap.

What happened

The Clearing House (TCH), the payments operator owned by 25 of the largest US banks, will run the network. It connects traditional rails (RTP, CHIPS) to blockchain infrastructure for 24/7 atomic settlement, with use cases spanning programmable treasury, real-time liquidity, cross-border payments, and agentic commerce. “A big move for the banks,” TCH CEO David Watson told the WSJ; the industry faces a “radically different” future in on-chain payments. The release names 17 participants, including BNY, HSBC, PNC, Truist, TD Bank, and U.S. Bank. One detail buried in the coverage: no blockchain partner has been selected yet. The build, in any meaningful sense, has not started. [RELEASE] [ANALYSIS]

The whole perimeter is mobilizing. In March 2026, five regional banks (Huntington, First Horizon, M&T, KeyBank, Old National) holding $600B+ in combined deposits launched the Cari Network on ZKsync, with a pilot set for Q3 2026. Eugene Ludwig, the former Comptroller of the Currency, founded it. In 2025, North Dakota partnered with Fiserv for a state-level token. The banking sector is fully mobilizing to keep enterprise capital strictly within the FDIC-insured perimeter. [NEWS]

The timing is no coincidence: The CLARITY Act cleared the Senate Banking Committee on May 14 carrying the Tillis-Alsobrooks compromise: stablecoins cannot pay passive, deposit-style yield, but rewards tied to actual usage stay legal. Banks wanted that loophole closed entirely. ABA members sent more than 8,000 letters to Senate offices. Jamie Dimon told crypto firms that want to pay yield to apply for banking charters. The TCH network is what banks build when lobbying stops working.

Why it matters

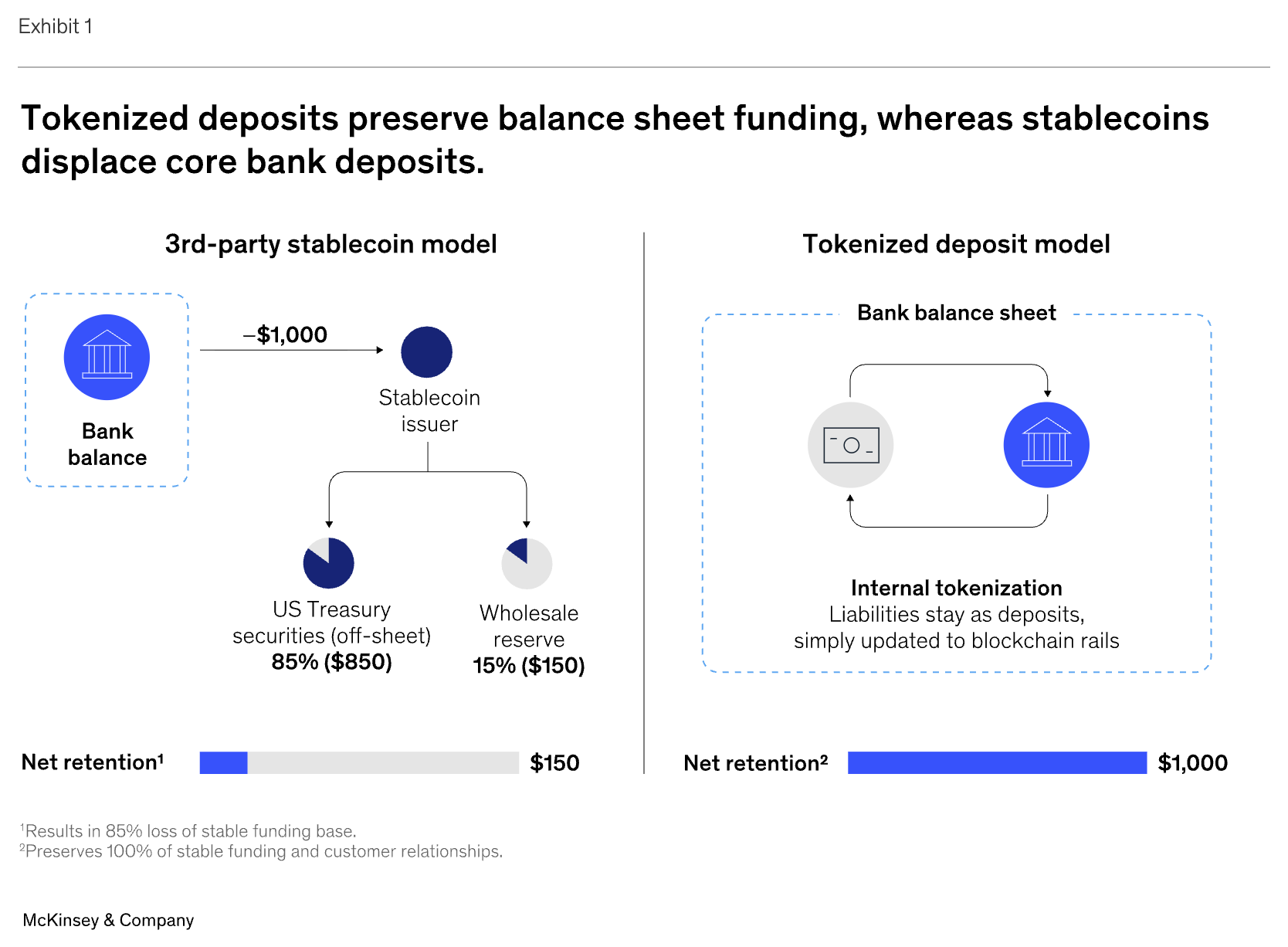

The deposit math: McKinsey modeled it in May: when a corporation moves $1,000 into a third-party stablecoin, only $150 returns to the banking system as wholesale reserves. The other $850 buys T-bills off bank balance sheets. Tokenized deposits keep the full $1,000 on the bank’s balance sheet, preserving credit capacity. The Bank Policy Institute went further on May 8. Applying an industry-sponsored model to the projection that stablecoins reach ~$4T by 2030, BPI calculates deposits would first rise by $300B, then fall by $4T. Net result: $3.7T in destroyed deposits and a 19% decline in bank lending. A December Fed note by Jessie Jiaxu Wang points the same direction: credit supply likely shrinks, lending costs likely rise.

Regulation drew the moat, banks are now paving it. The GENIUS Act (signed July 2025) bars stablecoin issuers from paying interest, taking deposits, or making loans, and excludes them from deposit insurance. Tokenized deposits sit on the opposite side of every one of those lines: they live inside the banking system as a digital representation of bank deposits, pay interest legally, carry FDIC insurance up to $250,000, and fund loans. A corporate treasurer choosing between two on-chain dollars faces a simple test: one yields and is insured, the other is neither. That test decides the enterprise layer.