Hey, it’s Marc.

I watched DTCC’s live updates on Wednesday like a product launch. In a way, it was one.

At 8:30am, JPMorgan converted QQQ shares into tokens. By late morning, it posted tokenized assets to meet a margin call at CME.

Real securities. Real margin. Live production.

DTCC just shipped what crypto spent a decade promising. Let’s unpack.

The Signal: This looks like a tokenized stocks story. It is a collateral story. The first thing Wall Street did with tokenized securities was post margin and move repo, because collateral is where minutes are worth money. DTCC now runs both versions of that machine.

53 seats remaining

197 executives have already registered for our next webinar. Attendance is capped at 250, and registration will close once capacity is reached.

I’ll be joined by the people advising banks on stablecoin strategy—and building the infrastructure those institutions will ultimately use.

Designed for CEOs, board members, and senior leaders across banks, financial market infrastructures, asset managers, and custodians.

📅 23 July, 11am EST

🚨 Reserve your place before registration closes.

What happened

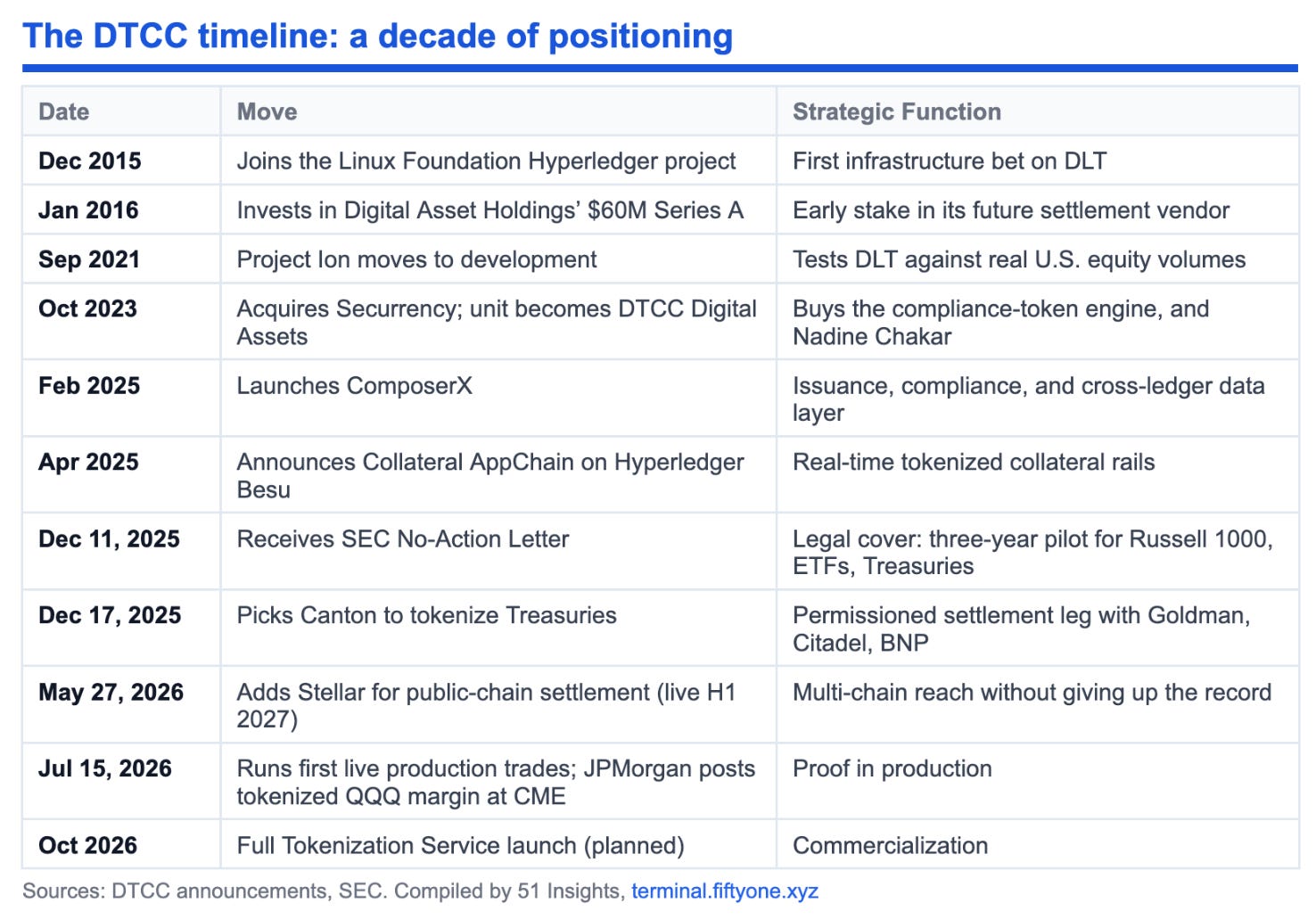

On July 15, DTCC converted securities held at its DTC depository into tokens and used them in live production trades. The firm calls it the largest tokenization production event yet by use cases, asset classes, and participants. More than 30 firms took part, including BlackRock, JPMorgan, Goldman Sachs, Vanguard, Citadel Securities, Circle, and CME Group. Trades settled on Hyperledger Besu, DTCC’s private network, and Canton, a public network built for regulated finance.

The workflows were pure back office: collateral pledges, securities lending, Treasury repo, equity trades, and clearinghouse margin. JPMorgan tokenized Invesco QQQ holdings, then posted tokens to meet margin requirements at CME. Societe Generale pledged tokenized Treasuries to Citadel Securities. Microsoft and Circle shares, SPY, and Treasuries across maturities were tokenized during the day.

These tokens are digital twins. Each one is the DTC-held security itself, with identical ownership, dividend, and voting rights, convertible back on demand. The event lands seven months after the SEC’s December No-Action Letter (our analysis) and eleven weeks before the full service launches in October.

Why it matters

Collateral is the product. Ignore the 24/7 stock trading headlines and look at what the banks actually demonstrated: margin, repo, securities lending, pledges. The U.S. repo market runs $12.6 trillion in daily exposures, and 69% of it is collateralized by Treasuries. DTCC’s own clearing arm, FICC, already handles $4.4 trillion of that every day. When collateral moves in minutes instead of hours, banks post less and free billions in capital. We made this call in December: speed, not slicing, is the payoff. Wednesday proved it in production. The first real use of a DTC token was a margin call.

Digital twins squeeze the wrapper issuers. A DTC twin is the security. Kraken’s xStocks and Robinhood’s EU tokens are synthetic claims on price exposure, and the SEC drew that line in writing in January. The wrapper firms saw this coming. Ondo joined DTCC’s working group and now builds distribution on top of DTC twins instead of competing with them. Once October gives allocators a choice between a claim on QQQ and QQQ itself, no compliance officer debates it.

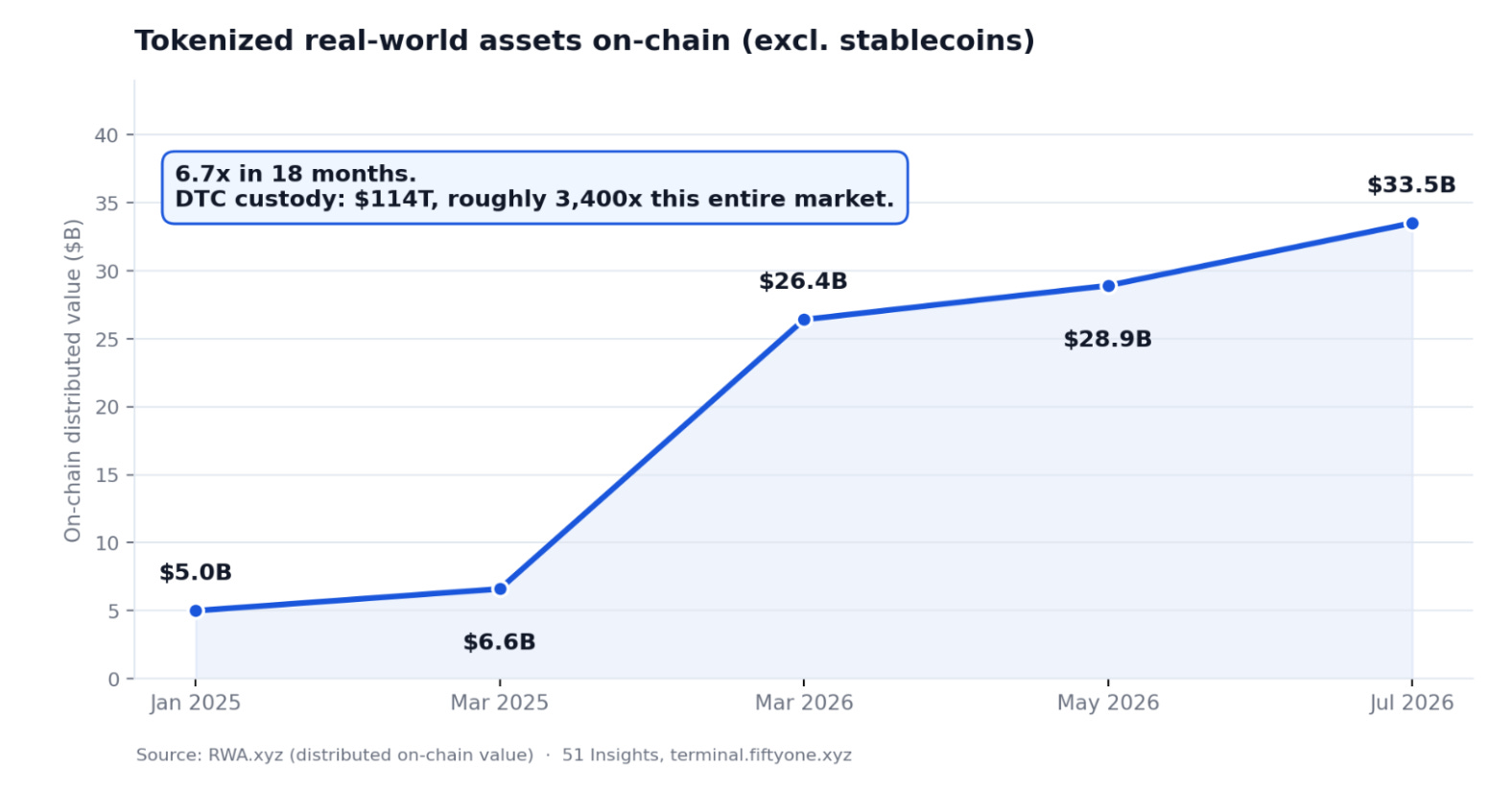

Tokenization has decoupled from crypto. Bitcoin trades near $65,000, roughly half its October peak. On-chain RWA value still hit a record $33.5 billion this month, up from $6.6 billion in March 2025, and DTCC’s working group grew past 100 members. This is an infrastructure cycle running on its own clock. “Crypto exposure” and “settlement infrastructure exposure” are now two different board decisions.

You know what happened. PRO goes deeper.

The complete member analysis examines:

Why DTC digital twins put pressure on synthetic token issuers

Which businesses gain and lose when the underlying security itself becomes tokenized

Why tokenization is now moving independently of crypto prices

What could prevent the October launch from reaching meaningful volume

Our take

PRO also includes the complete PDF, 4–5 weekly intelligence briefings, member research, events, and the full 51 archive.