Hey, it’s Marc.

Circle stock fell more than 12% on Tuesday, its worst day in four months, and I think most of the coverage is about to miss why. The trigger was Open USD, a new stablecoin from a group of 140 companies that includes Stripe, Coinbase, Visa, Mastercard, BlackRock, BNY and Google.

It’s built to do the one thing Circle does for a living: collect the interest on the reserves. Unlike USDC, it hands reserve income back to the businesses that distribute it and keeps only a management fee. The token is not live yet. The threat already is.

The Signal: Circle already pays out more than half its reserve income to keep USDC moving, mostly to one partner. Open USD’s real weapon isn’t sharing the float. It’s owning the distribution Circle has to rent.

PRO: Download PDF at the bottom

🚀 Build credibility. Drive pipeline. Win in digital assets. We position you as the authority among 100,000+ digital asset decision-makers who act on what we publish.

What Happened

A consortium of more than 140 companies launched Open USD on Tuesday, a dollar stablecoin issued by an independent entity called Open Standard. Founding partners include Stripe, Coinbase, Mastercard, Visa and BlackRock, alongside BNY, Standard Chartered, DBS, U.S. Bank, Shopify, Google, IBM, Klarna, Chime, Fireblocks, Anchorage, MetaMask, Aave, Solana, Polygon and Ripple.

The model goes straight at Circle. Partners mint and redeem without fees, and the reserve income flows back to the businesses using it, minus a management fee. No single issuer controls it; the members share governance. Zach Abrams, who co-founded Stripe-owned Bridge, runs it as interim CEO, and it goes live later this year. And notice who isn’t in the room: USDC, USDT and PayPal’s PYUSD.

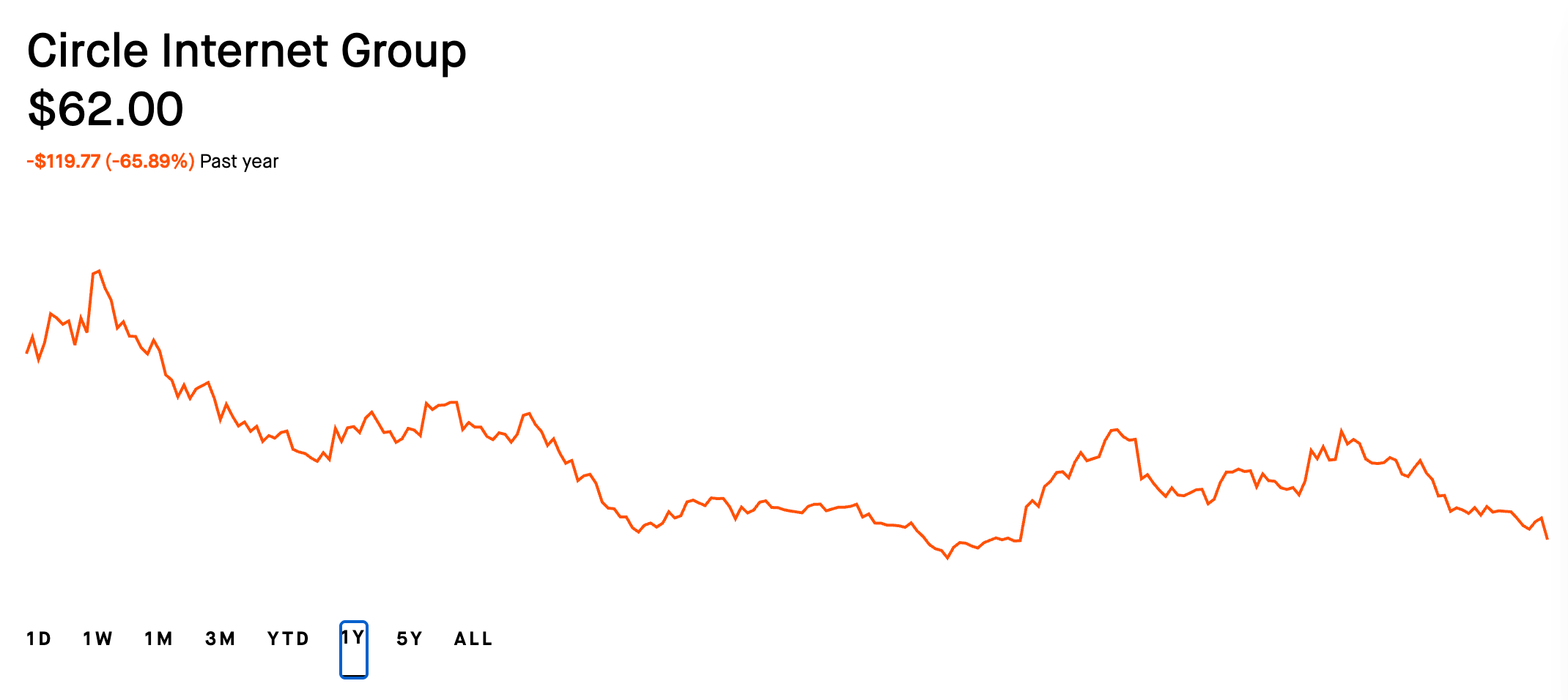

The market reacted fast. Circle (CRCL) dropped more than 12% to a four-month low near $66, down from a 52-week high of $263, and it did that on a day the Nasdaq rose. For scale: USDC sits around $73 billion and Tether’s USDT around $145 billion, the whole market is past $300 billion, and Citi thinks it reaches $4 trillion by 2030. And this isn’t the first time we’ve seen the move. Paxos already built USDG to split reserve income with Robinhood and Kraken, and a group of European banks did the same with a euro stablecoin called Qivalis.

Why It Matters

Circle’s moat was never the yield. It was distribution, and that just got attacked. Here’s what a lot of people don’t realize. Circle doesn’t actually keep the float. Coinbase takes 100% of the reserve income on any USDC sitting on its platform, and 50% of what’s earned anywhere else. Put numbers on it: in 2024, $908 million of Circle’s $1.01 billion in distribution costs went to Coinbase, about 54 cents of every dollar Circle made. And Coinbase’s slice keeps growing, from roughly 5% of USDC supply in 2022 to 22% by early 2025. So Circle is already renting its reach, from a single exchange. Now look at what Open USD brings: Stripe’s merchants, Visa and Mastercard’s networks, the banks, Shopify, Google. You can’t rent your way to that. Owning your distribution beats renting it.

The GENIUS Act was meant to be Circle’s moat. It became the on-ramp for everyone else. This one is almost ironic. Being regulated was supposed to be Circle's edge. But once regulation becomes the price of entry, Visa, Mastercard, BNY and the banks all issue on the exact same footing. The wall Circle was counting on turned into a door everyone walks through. And the Fed's mid-June proposal to put bank-style identity checks on issuers just raises Circle's costs without giving it anything its new rivals don't also have.

BlackRock wins no matter which token wins. This is our favorite detail, and it's the one the headline skips. BlackRock manages about 87% of USDC's reserves through the Circle Reserve Fund, and BlackRock is also a founding partner of Open USD. BNY custodies the cash today and will custody it tomorrow too. So whichever token you back, the same asset managers run the money and clip the fee. They're the house. The issuers are just fighting over a seat at the table.

In Their Words

Stablecoins represent one of the largest market opportunities in the world. We welcome continued innovation and competition and look forward to remaining laser-focused on building the best stablecoin infrastructure possible.

Jeremy Allaire, CEO, Circle, on X

Existing stablecoins have great strengths, but to use them at scale, businesses need something that’s open, low-cost, high-throughput, broadly accessible, and aligned to their interests.

Zach Abrams, interim CEO, Open Standard

The Big Picture

We think the float is being repriced from a private toll into a public utility, and Open USD is where that goes mainstream. Track the last nine months on the 51 Terminal and it reads as one story, not four: