who owns the agent economy?

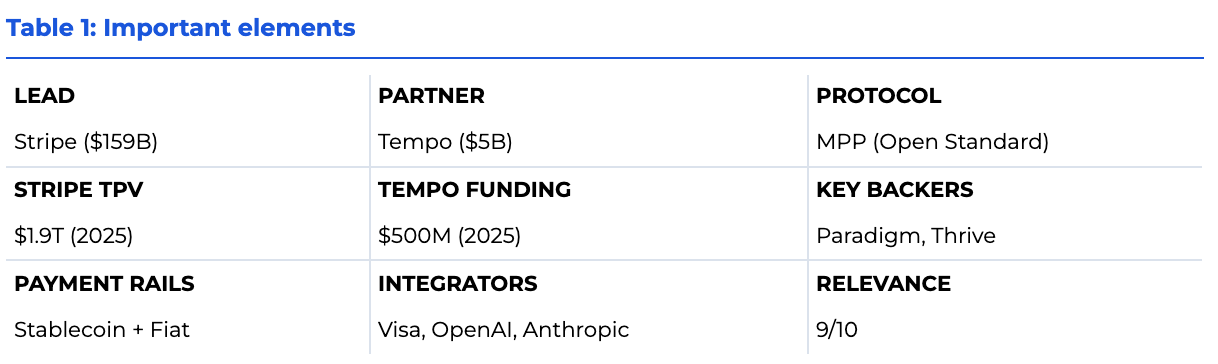

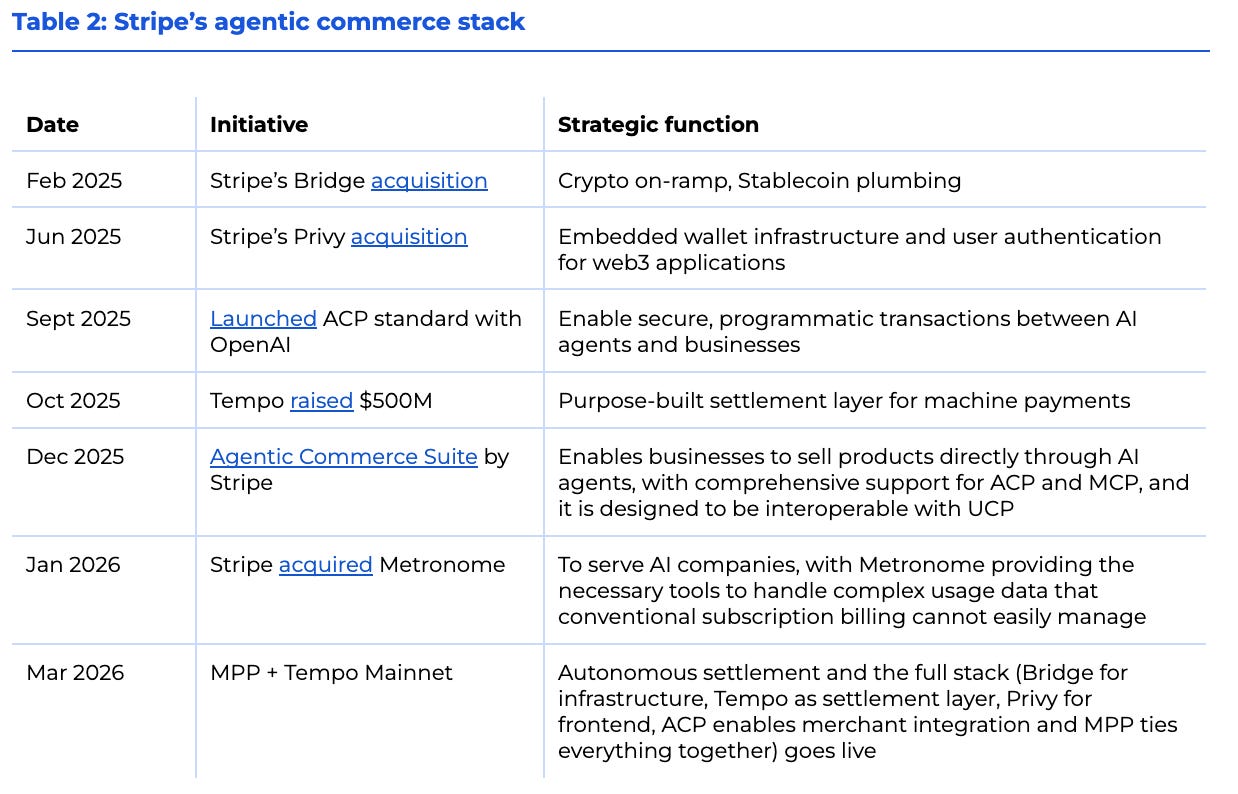

On March 18, 2026, Stripe and Tempo co-released the Machine Payments Protocol, an open specification for machine-to-machine payments.

Hey, it’s Marc,

The entire $10T global commerce stack was engineered for humans with credit and debit cards. Apple and Google have been extracting a 30% tax on the internet simply by owning the checkout screen for digital goods.

But, the next generation of consumers are not going to use screens or interfaces at all. We just entered the “Silent Economic Singularity.” AI agents now observe, reason, and crucially spend money autonomously. And, Stripe is building for them, combining stablecoins with AI agents with the Machine Payment Protocol. [RELEASE]

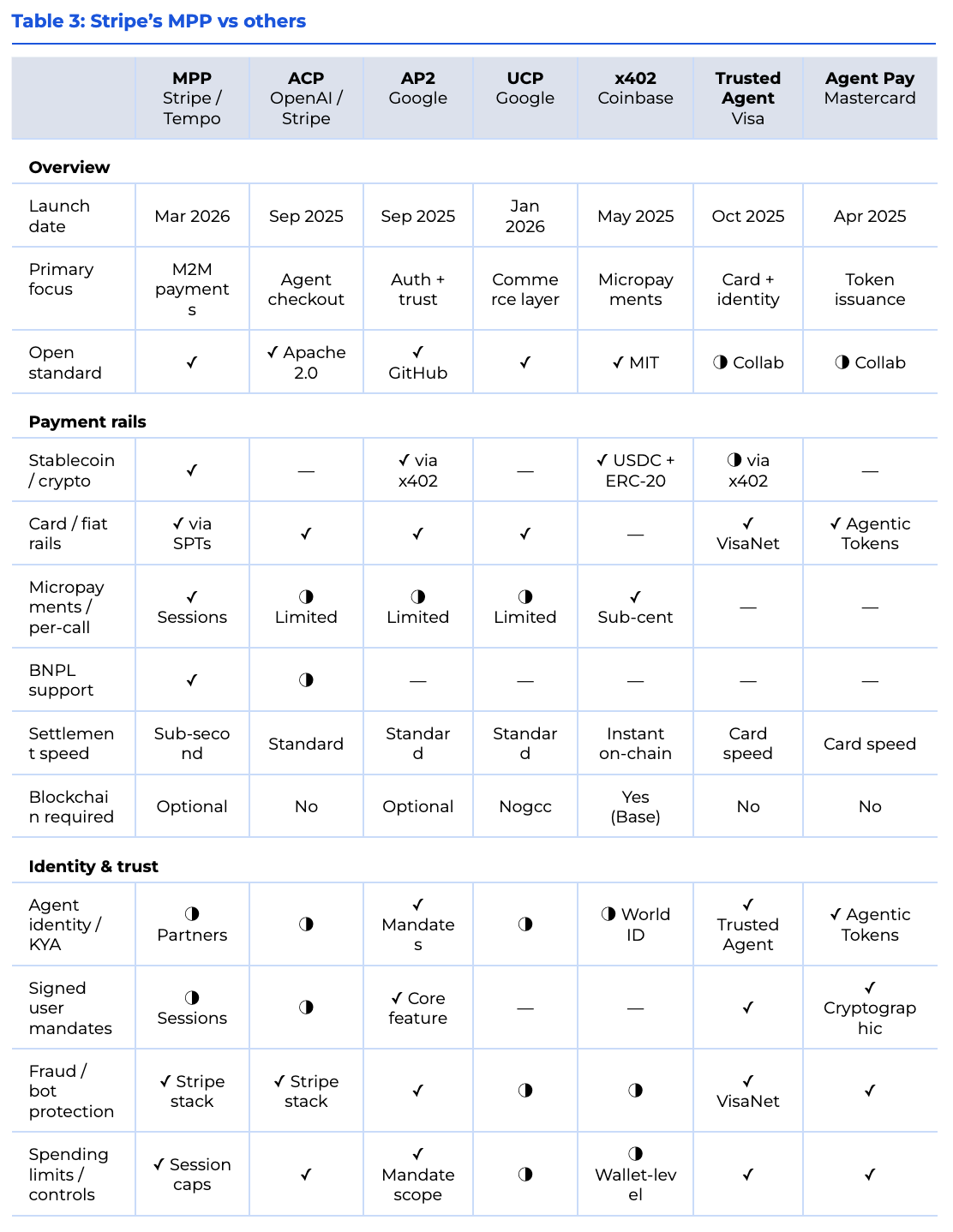

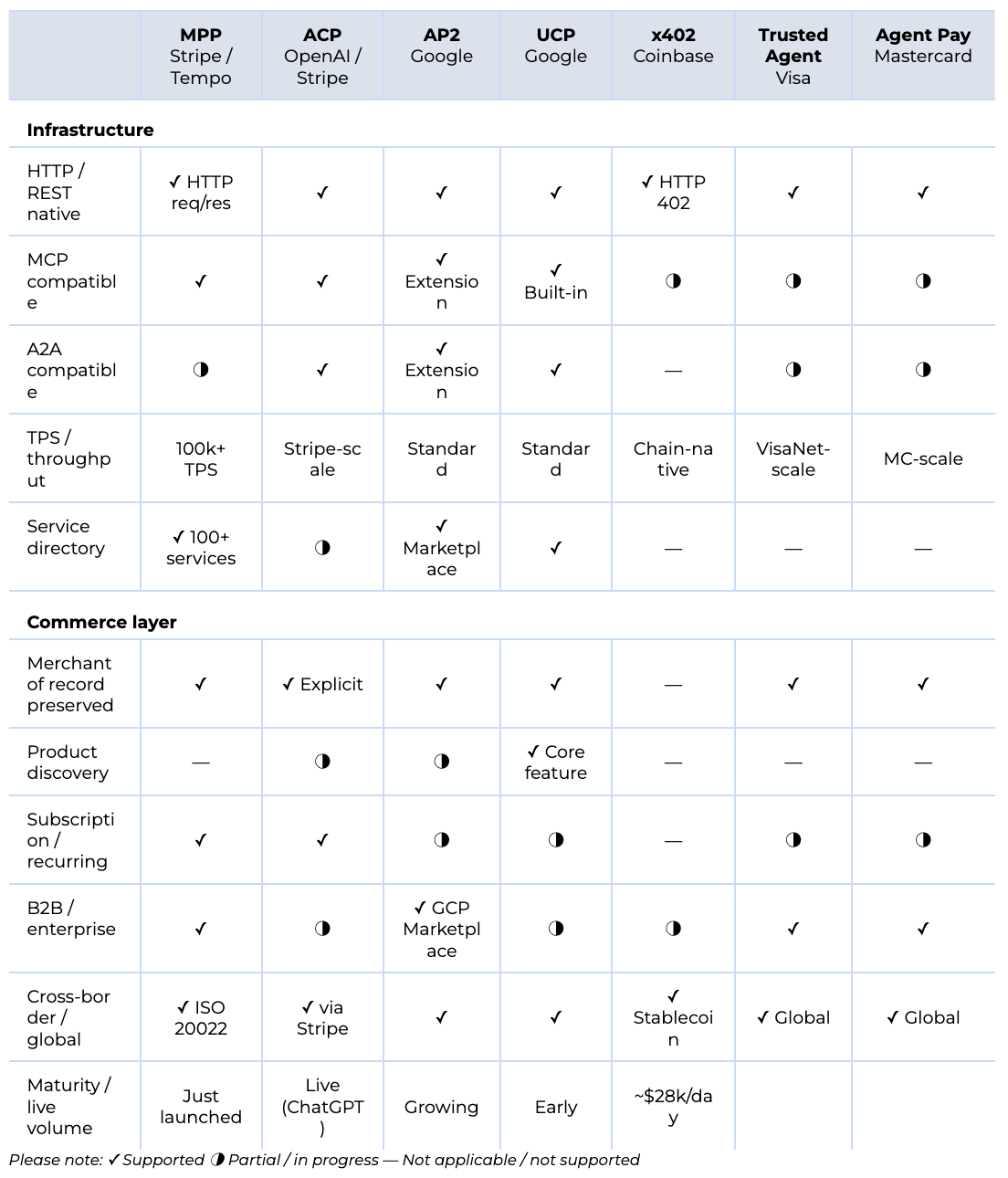

The Signal: The traditional App Store tollbooth is collapsing. The execution layer of the internet is shifting from human interfaces to machine-to-machine APIs. Stripe’s MPP is not the only one framework for A2A (agent to agent) payments. OpenAI and Google have been building separate frameworks: ACP and UCP simultaneously.

👉PRO: Download the PDF Reprot below

🚀 Build credibility. Drive pipeline. Win in digital assets. We produce institutional-grade research that positions you as the authority in your category, then distribute it to 100,000+ decision-makers who act on what we publish. Let’s talk.

What happened

On March 18, 2026, Stripe and Tempo co-released the Machine Payments Protocol, an open specification for machine-to-machine payments. Simultaneously, Tempo launched its mainnet, a purpose-built blockchain backed by $500 million from Paradigm, Thrive Capital, and other investors at a $5 billion valuation. [RELEASE]

It revives the dormant HTTP 402 “Payment Required” code: an agent requests a resource, receives a payment prompt, pays cryptographically, and unlocks access in milliseconds.

Zooming in: MPP supports both fiat and crypto. Stripe’s Shared Payment Tokens (SPTs) let agents pay via Visa, Mastercard, or BNPL on a user’s behalf, without exposing card data. Tempo settles the stablecoin leg with sub-second finality and tens of thousands of TPS. Early live deployments include Browserbase (cloud compute), PostalForm (AI-to-physical mail), and Prospect Butcher Co. in New York City, which now accepts sandwich orders from AI agents.

Competitive landscape

The agent payment landscape in 2026 is converging around three distinct but complementary layers.

Payment rail layer: Stripe’s MPP and Coinbase’s x402. Low-level primitives for actually moving money between machines, with MPP covering both fiat and stablecoins at 100k+ TPS via session-based authorization, and x402 embedding sub-cent USDC payments directly into HTTP requests

Trust and authorization layer: Google AP2, Visa Trusted Agent Protocol, and Mastercard Agent Pay. They don’t move money themselves but define who an agent is, what it’s allowed to spend, and how that mandate is cryptographically signed and revoked.

Commerce layer: OpenAI ACP and Google UCP. They handle product discovery, checkout UX, merchant-of-record rules, and the structured negotiation between a buying agent and a selling service.

In practice, these layers stack rather than compete: a transaction might use AP2 mandates to authorize an agent, MPP to settle the payment, and ACP or UCP to structure the commerce interaction around it, which is why Stripe, Google, Visa, Mastercard, and OpenAI are all listed as design partners on each other’s protocols.

The most likely outcome is a split: regulated commerce stays on card rails, while machine-to-machine payments; agents hiring agents, paying per API call, buying compute on demand, migrate to stablecoins because the economics demand it.