Fidelity doesn't do crypto. It manages $6.8 trillion. So when the 79-year-old asset manager launched its own stablecoin on January 28, the game fundamentally changed.

On January 28, 2026, the second-largest asset manager in America launched FIDD, a dollar-pegged stablecoin that Fidelity issues, distributes, and custodies in-house. [PRESS RELEASE].

For the first time, a titan with a national trust bank charter, the highest tier of federal oversight, is offering 24/7 dollar settlement on Ethereum. Let’s unpack.

👉PRO: Download the PDF below

What happened

Fidelity Digital Assets, National Association (a federally chartered national trust bank and a G-SIFI) launched FIDD: a 1:1 USD-backed stablecoin, live on Ethereum mainnet. Eligible customers can buy or redeem directly through Fidelity platforms, with daily disclosures of reserves, a transparency standard that exceeds rivals like Circle (USDC) and Tether (USDT).

Be smart: By using a national trust bank structure, Fidelity bypassed state-by-state money transmitter licensing, opting instead for direct OCC oversight. The token reserves sit in cash, short-term Treasuries, and qualifying repos. Listing on major exchanges is expected.

By the data: As of January 2026, stablecoins hit $316 billion in market cap with $45 trillion in annual transaction volumes, dwarfing Visa’s $14 trillion in fiscal 2025.

Zooming in: Fidelity has completed full vertical integration. The Fidelity Digital Assets bank issues the token. At the same time, Fidelity Management & Research (FMR) manages the reserves in-house. Unlike competitors like Circle and Paxos, Fidelity combines FIDD with its tokenized money market fund, the Fidelity Treasury Digital Fund (FYHXX). This pairing creates an internal liquidity engine, acting like a shadow central bank.

When clients need cash, Fidelity automates the redemption of yield-bearing FYHXX shares. It instantly mints FIDD against Treasury collateral. This setup allows for flexible, 24/7 liquidity. It effectively turns US sovereign debt into private digital currency. This all happens within a closed system, avoiding the T+1 settlement delay of traditional banking.

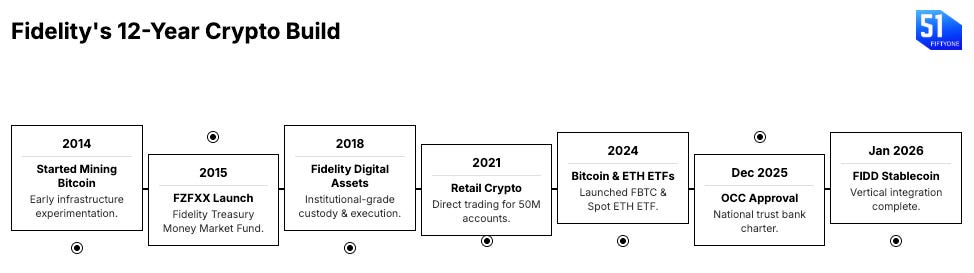

Stepping back: Fidelity has been building crypto infrastructure for over a decade, and each step created what they needed to run a FIDD stablecoin business from top to bottom: secure storage, trading systems, regulatory approvals, and distribution channels.

Zoom out: The $316B stablecoin market is a duopoly shaped by regulatory differences. Tether (offshore/high-risk) holds $187B. Circle (onshore/compliant) has $72B. Fidelity’s entry brings together Tether’s integration and Circle’s compliance and distribution. The nationally chartered trust bank lets stablecoins be issued across the country. It doesn’t require state licenses. Federal oversight covers reserves, and there are clearer rules for digital assets.

The GENIUS Act stops Circle and Tether from competing with bank deposit rates. It also prevents large outflows from the banking system. This setup boosts Fidelity’s ecosystem advantage. Clients can hold FIDD for instant settlement and then move to Fidelity’s tokenized money market funds when they want yield.