Hey, it's Marc.

I always assumed crypto would tokenize Wall Street. Turns out Wall Street is doing it itself. DTCC settles every U.S. equity and Treasury trade, holds $100T in custody, and once cleared $5.55T in a single day. In H2 2026, that plumbing goes on-chain with the SEC's blessing. Let's get into it. [ARTICLE]

The Signal: DTCC is attempting to build a structure for tokenization on legal infrastructure that already works. This is an American infrastructure upgrade from the inside.

👉 Join our webinar: The End of the Seed Phrase, with Dmitry Tokarev, founder of Copper Technologies (one of the largest institutional crypto custodians in the world) and now founder of Bron Labs, backed by GSR, and ~140 other investors.

What happened

DTCC has been quietly assembling the pieces for two years. In April, it told the market what it built.

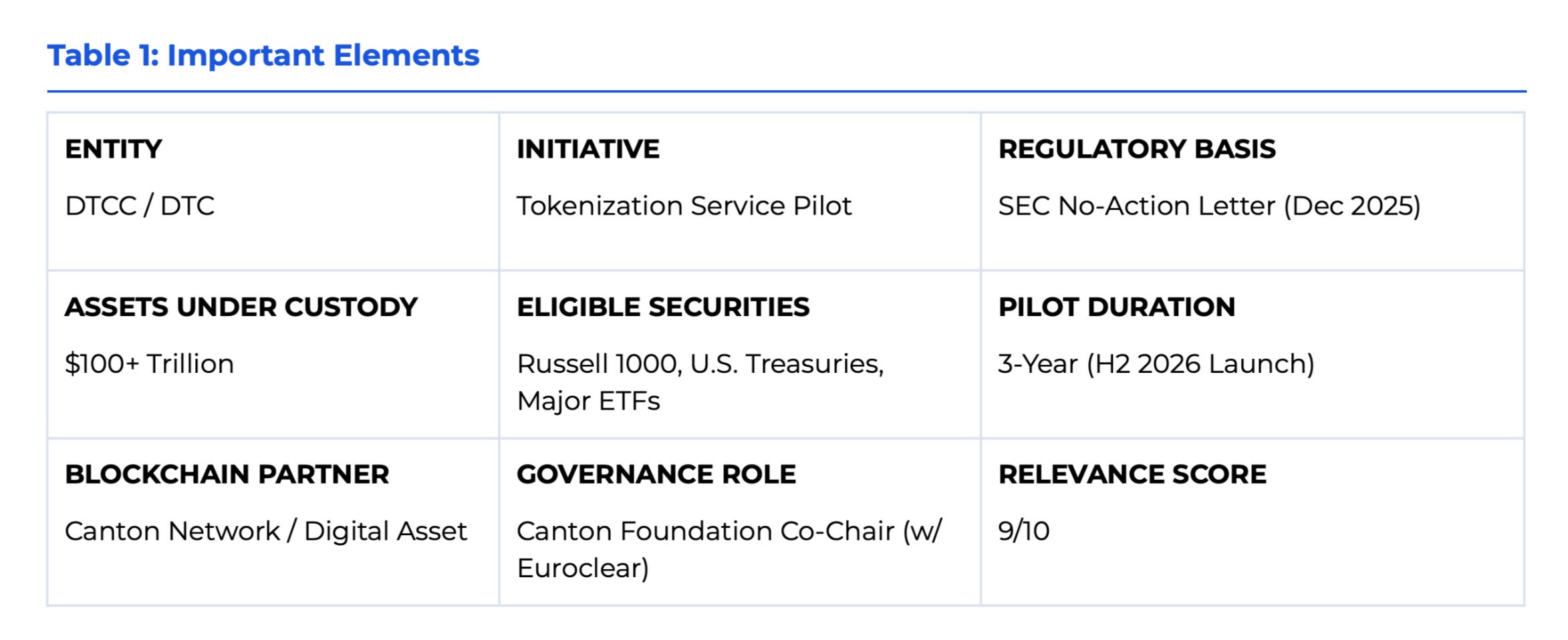

It started with a December 2025 SEC no-action letter granting DTC a three-year exemption from Reg SCI, Section 19(b) rule-filing requirements, and key clearing standards under Rules 17Ad-22 and 17Ad-25. That cleared the regulatory path. [RELEASE]

In March 2026, the House Financial Services Committee held its hearing on tokenized securities, and DTCC Deputy General Counsel Christian Sabella filed written testimony the same day.

By April 13, DTCC had published its public-facing roadmap. The pilot launches in H2 2026.

What he said, translated:

DTCC supports tokenization. → DTCC is going to run tokenization.

Innovation must build on existing legal frameworks. → No new asset class, no Wyoming-style rewrite, securities law still applies.

Multilateral netting must remain a key benefit. → Atomic bilateral settlement isn’t compatible with how Wall Street actually works. Drop it.

Tokenization will lead to a hybrid evolution where different assets use different models. → Equities and Treasuries stay in DTC’s pool. Private debt and the long tail can go on-chain natively.

Interoperability is the make-or-break issue. → Don’t build your own chain. Build on ours, or connect to ours.

Tokenized securities must carry the same rights as today’s assets. → The wrapper can be programmable. The substance can’t change.

The service will be voluntary and protocol-agnostic. → DTCC won’t pick Ethereum or Canton or Polygon. It’ll be the connective tissue between all of them.

Innovation should strengthen, not erode, investor protections. → Pre-approved wallets, reversible entries, KYC at the ledger level.

Lasting market evolution comes from coordinated industry action, not technology alone. → Solo crypto-native protocols don’t get to set the rules.

Done right, tokenization helps DTCC carry its mission forward. → DTCC plays offense in this transition, not defense.

Table 1: Important Elements

The three takeaways that matter

DTCC is positioning itself as the standards body. “Interoperability” sounds neutral. Read it again. It’s DTCC saying every tokenization effort either plugs into its plumbing or eats fragmentation costs. That’s a warning, dressed as an industry value.

Netting is the red line. Sabella named multilateral netting twice as a benefit that must remain. This is the tell. Any tokenization model that breaks netting, including atomic bilateral settlement and on-chain repo without a CCP, is incompatible with this regime. Half the crypto-native architecture in the market just got put on notice.

Hybrid evolution is permission, not prediction. The line about different assets using different models is DTCC drawing a map. Equities, Treasuries, and ETFs run through DTC’s tokenized rails. Private equity, real estate, and structured credit can issue on-chain natively. The crypto-native firms got the long tail. DTCC kept the core.

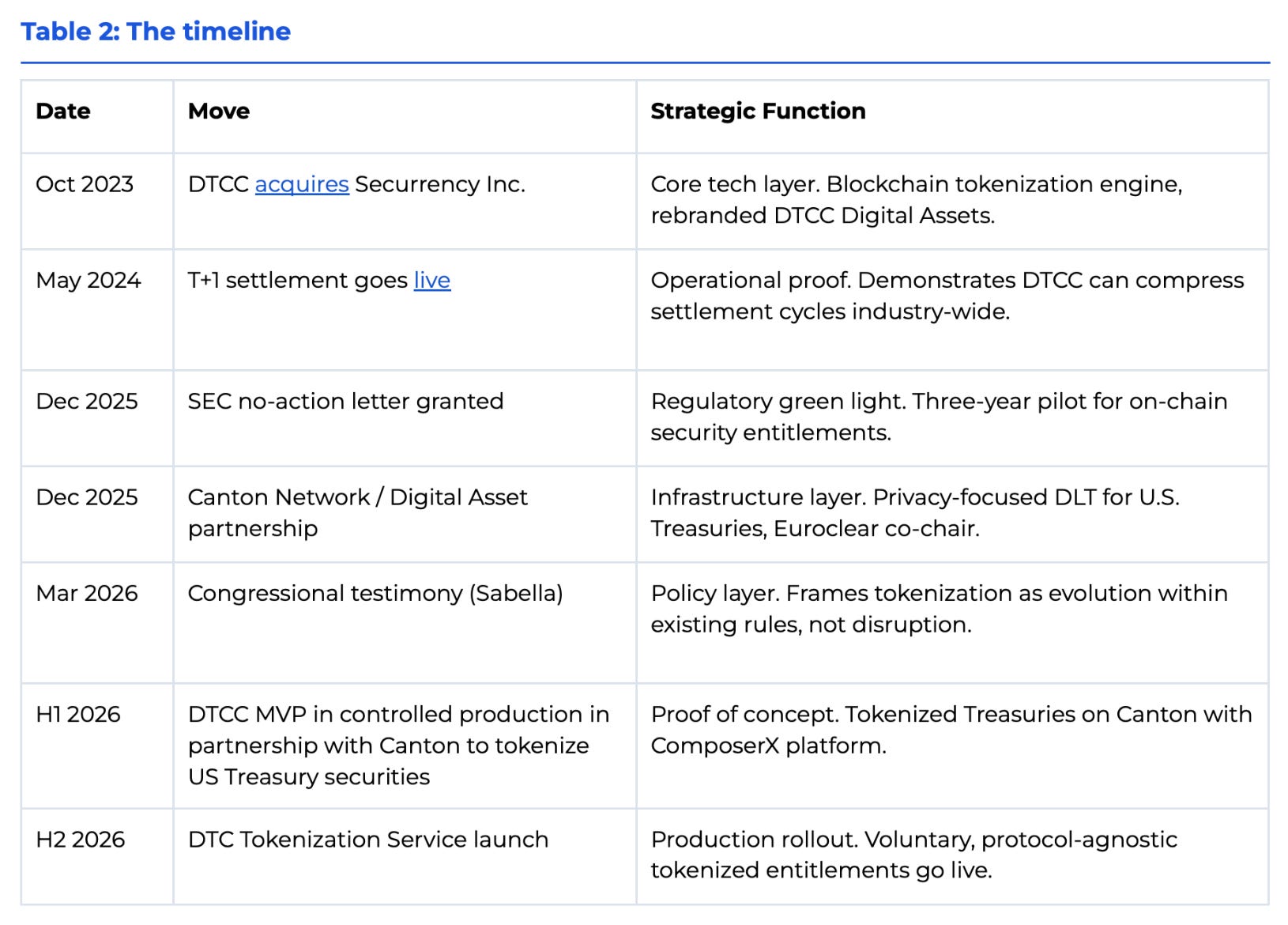

Table 2: The timeline

Why it matters

Sabella’s real message: we will tokenize Wall Street, but on our terms. The testimony’s most important word was not “tokenization,”it was “interoperability.” Sabella made a specific argument: tokenization efforts built in “isolated or proprietary environments risk fragmenting liquidity and increasing cost.” DTCC is warning against a world where every bank, exchange, and fintech builds its own tokenization silo. The alternative DTCC is proposing is itself, an open, protocol-agnostic infrastructure layer where tokenized securities inherit the legal protections, netting benefits, and settlement guarantees that exist today and hence acting as the connective tissue between every tokenization effort on Wall Street.

A huge implication for vendors: DTCC has refused to pick a chain. It is telling Ethereum, Canton, Polygon, Avalanche, and every enterprise DLT the same thing, that outcome is everything. Whereas, it puts walled gardens on notice. Proprietary consortium chains, single-issuer DLTs, and integrated tokenization stacks face a clear message that interoperability is the public good and fragmentation is the barrier to scale.

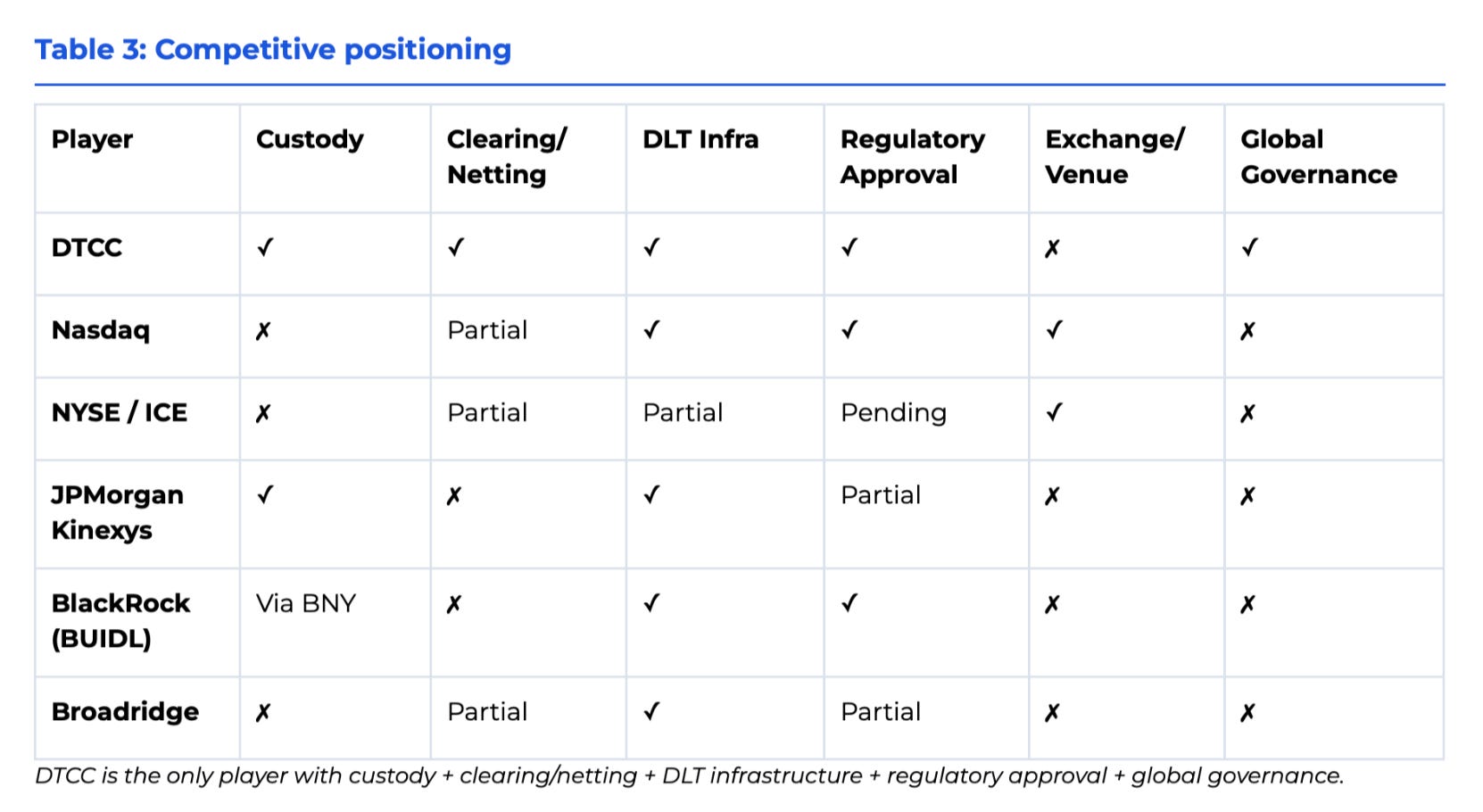

Table 3: Competitive positioning

Our take

For years the crypto pitch was that decentralized rails would replace DTCC. What’s happening instead is that DTCC is becoming the rails.

The mistake was thinking tokenization would bypass the incumbent. It doesn’t. It makes the incumbent more valuable. Multilateral netting compresses trillions in daily flow into a few billion in actual settlement. Atomic bilateral settlement breaks that math. Banks can’t afford to break that math. So whoever offers tokenization with netting intact wins. That’s DTCC.

Read the fine print on the pilot. Wallets must be pre-approved. DTC can reverse erroneous entries. The chain is programmable but the central ledger stays put. This isn’t the crypto-native vision wrapped in regulation. It’s the regulated system wrapped in crypto-native tech.

This makes DTCC an architect of tokenisation in the U.S. capital markets.